SquishTrade

@t_SquishTrade

Ne tavsiye etmek istersiniz?

önceki makale

پیام های تریدر

filtre

SquishTrade

بیت کوین روی ابر ایچیموکو حمایت شد: آیا زمان برگشت فرارسیده است؟

BTCUSD 6 Ekim 2025'teki yeni ATH'dan bu yana son iki aydır düzeltme modunda. Kısa vadeli basit ve üstel hareketli ortalamalar da dahil olmak üzere çeşitli teknik desteklerden düştü. Ancak haftalık zaman diliminde uzaklaştırma yapıldığında tam da olması gerektiği yerde destek buluyor gibi görünüyor. Ichimoku grafik sisteminde (Japonya'da geliştirilen denge tabanlı bir sistem), bulut desteği özellikle haftalık ve aylık grafikler gibi daha yüksek zaman dilimlerinde özellikle önemlidir. Ayrıca, yukarı doğru eğimli ve dar olmayan yeşil renkli bir bulut, yükseliş eğilimini ve daha güçlü desteği gösterir. Tabii Kijun hattı haftalık olarak yukarıdan geçiyor. Daha fazla yükseliş için bunun önümüzdeki birkaç hafta içinde aşılması gerekiyor. Standart ayarlarda Bollinger Bantlarının uygulandığı aylık grafik, BTC'in bu değişken konsolidasyon ve düzeltme döneminde basitçe ortalamaya geri döndüğünü ortaya koyuyor. İşte bir anlık görüntü: Her zaman kendi araştırmanızı yapın ve riskinizi pozisyon boyutunuza uygun şekilde yönetin! Ve tatil sezonunun tadını çıkarın. Herkese Mutlu Noeller ve Mutlu Yıllar!

SquishTrade

All Eyes on Critical Support for Bitcoin!

Tüm gözler şimdi yukarıdaki birincil grafikte gösterilen BTCUSD 'nin bayrak desteğini izliyor olmalı. BTC'nin tüm zamanların high seviyesi 73.794 dolardan beri, BTC genellikle boğa bayrağı olarak adlandırılan aşağı eğimli bir bayrak kanalına uyan istikrarlı ancak değişken bir konsolidasyon modeline sahipti. Ancak alt kanal kesin bir şekilde kırılırsa boğa bayrağı artık boğa bayrağı değildir. Bu yüzden tüm gözler şimdi bu desteğe çevrilmiş durumda. İlginçtir ki, yukarıdaki birincil grafikteki sarı çizgi 51.985 dolarda bir Fibonacci .618 geri çekilmesidir. Bu .618 geri çekilmesi bir dereceye kadar bugünkü bayrak desteğiyle örtüşmektedir. .618 geri çekilmesi, alçalan kanalın dönüş çizgisiyle birlikte destek sağlayamazsa, one en azından 23 Ocak 2024'teki büyük salınım düşüklüğünü yeniden test etmek için daha düşük fiyatlar bekleyebilir. Jeopolitik çatışmanın tırmanmasıyla birlikte fiyatlar normalden daha oynak olabilir. Bu, destek/direnç sınırlarının daha kolay kırılabileceği anlamına gelebilir. Ve yanlış yükselişler ve düşüşler daha şiddetli ve baştan çıkarıcı olabilir. Bu yüzden dikkatli olun! Rahatlatıcı yükselişler gerçekleşse bile, fiyat gelecek yıla kadar mücadele etmeye devam edebilir. Ancak kimsenin tahminlerine güvenmeyin -benimkiler dahil! Objektif, tarafsız kalmaya çalışın ve fiyatın size ne söylediğini izlemeye devam edin -varsayımlarınızı fiyat hareketine zorlamaya çalışmadan. Başka bir deyişle, fiyatın bir hafta sonra, bir ay sonra, bir yıl sonra ne yaptığı, size hemen hemen her yatırımcının veya teknik analistin söyleyebileceğinden daha fazla bilgi verecektir. Son olarak, fiyatın bu bayraktan/kanaldan daha fazla kırılması durumunda izlenebilecek bazı uzun vadeli seviyeler şunlardır.

SquishTrade

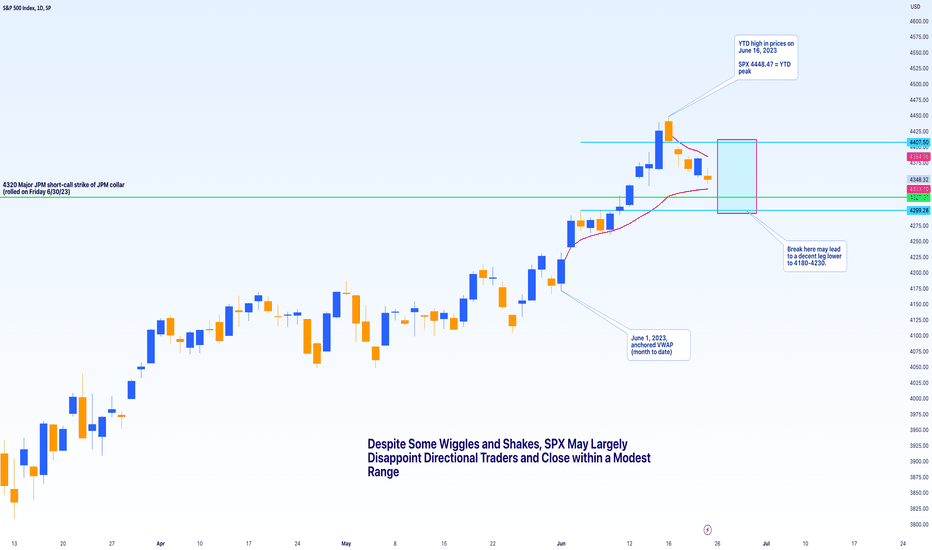

Despite some wiggles and shakes, SPX may disappoint this week

Birincil Grafik: SPX Anahtar seçenekler-OI seviyesine (JPM'nin üç aylık yakasıyla ilgili) ve bu hafta izlemek için birkaç önemli VWAP ile günlük zaman çerçevesindeki grafik. Hafta için destek ve direnç mavi yatay çizgilerle gösterilmiştir. SPX, agresif beslenen yetkililerin yorumu tarafından ürkütülmedikçe veya FOMC beyanından şahin görüşlerini sulandıran ve 14 Haziran 2023'te verilen arsalar tarafından teşvik edilmedikçe, bu hafta mütevazı bir aralıkta ticaret yapabilir. SPX'in 2023'ünün ortasından bu yana, fiyat büyük ölçüde 4300 s 'a mütevazı bir şekilde düştü. Bu Haziran ortasındaki zirveden demirlenmiş VWAP'ın altında kaldı. Bu, sadece bu hafta (bu yazı adresleri) değil, aynı zamanda gelecek hafta ve Temmuz ayına kadar direniş izlemek için yararlı bir seviyedir. Şimdilik, destek, JPM'nin üç aylık yakasının kısa çağrı grevi olan 4320'nin (önemli çağrı gaması olan) büyük seçenek seviyesinde yatıyor. Bu yaka Cuma günü bu bilgileri dikkatlice izleyen seçeneklere ve VOL uzmanlarına göre yuvarlanacak. Önde gelen bir aracılıktan haftalık beklenen move yaklaşık 57 puanla verilmiştir. Bu, 4291 ila yaklaşık 4405 aralığına eşittir. Haftalık beklenen move için 16-Delta hesaplaması biraz daha geniştir ve 4278-4410 $ 'lık bir move aralığını göstermiştir. 30 Haziran'ın sona ermesi için IV kullanan bir diğer hesaplama, 4260-4428'deki diğer iki aralıktan biraz daha geniştir. Hacim profili bile beklenen hareket aralığına denk geliyor gibi görünüyor. Ek grafik A: Neden bu beklenen move rakamları bu hafta kullanıyorsunuz? Mükemmel değiller, ancak TA da değildir ve bazen, özellikle opsiyon riskten korunma akışlarının eyleme hakim olabileceği bir zamanda yardımcı olabilirler - Fed gerçekten tutarsız bir şey yapmadıkça (fiyatları beklenenden biraz daha uzağa itebilir) veya Prigozhin / Putin saga göründüğü kadar çözülmez (tamamen bilinmeyen). Bu, bilinmeyen siyah-denizlerin özellikle sosyal medyada gizlendiği, ancak neredeyse hiç gerçekleşmediği diğer haftalardan farklı değildir. Bu nedenle, fiyat tarafsız kalırsa yönlü tüccarlar büyük ölçüde hayal kırıklığına uğrayabilir. Bununla birlikte, verimliliğe ve çevik hassasiyete sahip yönlü yatırımcılar, onay ve risk yönetimi olan kurulumlar için sabırlı olabilmeleri koşuluyla, intraday veya haftalık aralıkların kenarlarında fırsatlar bulabilirler. Bununla birlikte, bu bir öneri değildir, ancak RangeBound Piyasaları bazen en iyi yalnız kalır. Ünlü ticaret hattını uzun sürecek bir zaman, kısa sürme zamanı ve balık tutma (veya başka bir saptırma) gitme zamanı hatırlayın. Her halükarda, bu tür piyasalar kısa vadede ticarette bir avantaj için en iyi umut, fiyat tezgahı ve bir tersine çevirmeyi onayladıktan sonra kenardan (major destek ve herhangi bir aralık için direnç) ticaret yapmaktır. Kısacası, para üreticileri bu hafta için tüm olasılıkla premium satıcılar olacak. Yukarıda açıklanan JPM kısa yakalı greve ulaşmanın yaklaşık 8-9 puanı içinde geldi. JPM kısa yakalı grev hafta için destek oldu. Yukarıda özetlenen beklenen hareket aralığı, bu hafta Perşembe gününe kadar 4/5 gün boyunca güçlü bir şekilde devam etti. Cuma günkü fiyat eylemi, beklenen PCE enflasyon baskısından biraz daha zayıf bir şekilde daha yüksek bir boşlukta şortun sıkıldığı için aralığın üst ucundan geçti. Yukarıda verilen farklı beklenen move hesaplamalarına bakarken, fiyat bu aralığın daha geniş versiyonunun (4260-4428) üst ucunun sadece yaklaşık 23 puan üzerinde kapanmıştır. "Önde gelen bir aracı kurumdan haftalık beklenen move yaklaşık 57 puanla verilir. Bu, 4291 ila yaklaşık 4405 aralığına eşittir. Haftalık beklenen move için 16-delta hesaplaması biraz daha geniştir, 4278-4410 $ 'dan daha geniş bir hesaplama, 420 $' lık bir şekilde 42.

SquishTrade

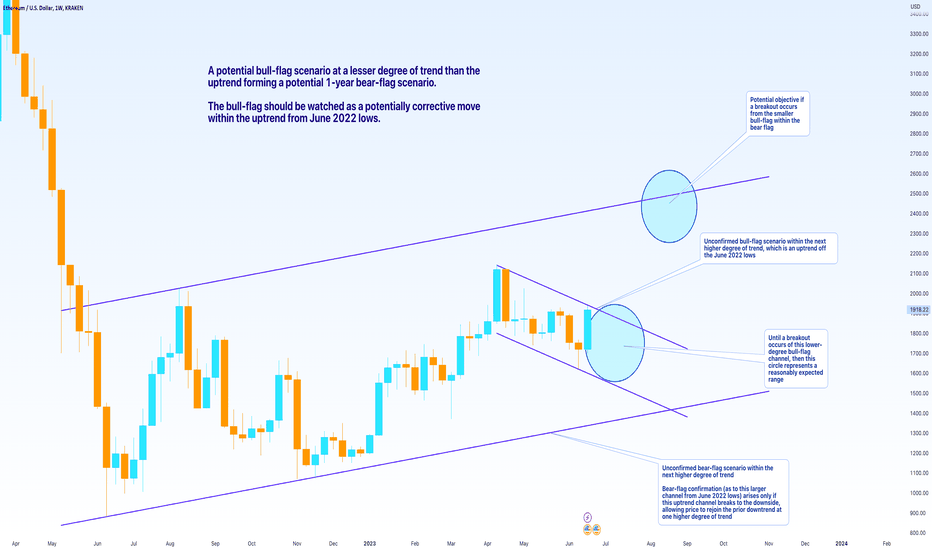

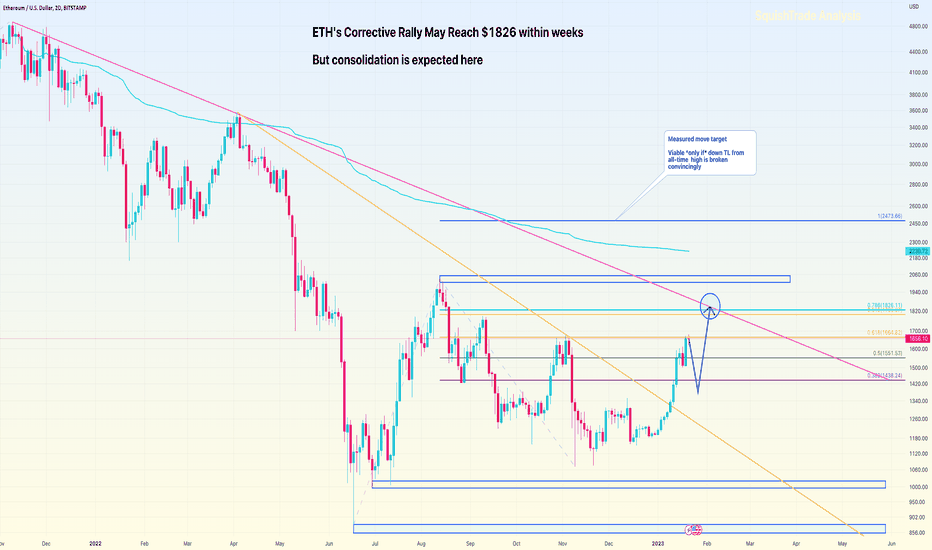

ETH's Nested Flags: Bull Flag within a Bear Flag

Primary Chart: Weekly Candle Chart of ETH/USD with Competing Flag Scenarios Longer-Term Analysis ETHUSD has been largely in a trading range since making its low in June 2022. Yes, some of the moves within that range have been quite substantial. The move off the June 2022 low to the early August 2022 high was about +130.59% higher. The next leg higher from the early November 2022 low to the April 2023 high was about a +99% move. In between those moves was a substantial -47.29% downdraft. (Downdrafts may have quite a smaller percentage because the starting point begins much higher than the starting point for an up move.) But big volatility, huge moves, don't guarantee a strong trend either way. A stock can chop up and down in a volatile way while its overall progress remains relatively insignificant given the volatility and moves. Consider the 1-year uptrend on the Primary Chart. The trend does not form a powerful, steep upward slope, moving sharply higher for many weeks consecutively like other charts we have come to see in recent months, e.g., NVDA, AAPL. Instead, the trend has largely been sideways with a modest uptrend with only a gradual incline despite the big moves within this well-defined channel. This could be a bear flag, though that is not yet confirmed. It's a scenario in any case that should be kept in mind on a break of the upward trendline from June 2022 lows. 1. Bear-Flag Scenario: Chart A (also shown on the primary chart) Notice how the VWAPs confirm the largely sideways ranging action. The VWAP from the all-time high and the VWAP from 2022 lows have been containing the price action YTD in 2023. Despite the gentle uptrend slope, the anchored VWAP from the all-time high reminds us of a more dynamic and flexible measure of trend, which is down from the all-time high in 2021. 2. Anchored VWAP from All-Time High: Chart B The anchored VWAP from the all-time high remains formidable to price. Notice is power in resisting price up until now. However, the last rejection did not send price to new lows. This confirms the choppy sideways thesis for now. While the dark-blue VWAP from the ATH did reject price in April 2023, price has remained well above the anchored VWAP from the major June 2022 low. Currently, the ATH-anchored VWAP lies at $2,038. A close above this level suggests at least further upside in the near term. Traders of all time frames should keep this area in mind—it's sort of like a super-highway. You don't want to run out in the middle of it without looking carefully both ways. The measured-move area is also shown here. Note that this is a logarithmic chart, so the measured move is somewhat higher than on a linear chart. This post will attempt to display measured moves on both. 3. Three Anchored VWAPS from Key Pivots: Chart C The anchored VWAPs on this chart confirm the consolidation thesis discussed above. The VWAPs are anchored to key swing lows and highs since the all-time high. NOtice how the VWAPs from these various pivots have been compressing and flattening for months. This signifies another major trend move is likely to occur when this long-term consolidation completes. Many hope it will be an upward move back to highs. SquishTrade is less confident of that conclusion given inverted yield curves (see prior posts on this); however, over the coming weeks, maybe months, choppy to somewhat higher prices can occur. 4. Triangle Patterns within Triangle Patterns: Chart D Triangles are consolidation patterns. The fact that we see triangle patterns within triangle patterns supports the idea that this 1-year channel is potentially consolidative of the move that preceded it. No guarantees, but that seems to be a logical inference. Some might counter that this is a major "cup base" though others may struggle to see anything resembling something that might hold one's tea. We'll see. Note: This is a linear chart, with a measured move based on the linear scaling. 5. Triangle pattern on a Logarithmic Chart: Chart E This chart shows a triangle on a logarithmic scale. So now, switching to log scale doesn't necessarily change the thesis just yet. The measured move for the log scale gives a 1-year measured move off of June 2022 lows around $2467. If we extend the measured move to a 1.272 projection of the first leg off the June lows, then it runs up around $3000. Long-term view summarized: As long as the uptrend from June 2022 lows holds, as well as the VWAP from that same bar, price can continue to remain supported, i.e., not crashing, sideways, rallies and dips within the defined ranges. In SquishTrade's view, $2,400 - $3000 is likely the maximum level ETH may achieve between now and the likely recession foretold by the yield curves. But higher-for-longer monetary policy in major European and North American countries may keep the ceiling even lower than that. Caution is warranted unless / until certain persistent (and 40-year record) yield curve inversions have proven that they finally gave a false signal for the first time ever. Shorter-Term Commentary Directional traders may be disappointed in the coming 2-3 weeks. A flag within a flag suggests more choppy price action overall—at least until a breakout of either occurs. The smaller flag may breakout first to the upside and lead us to the upper edge of the channel. The larger flag may breakout to the downside, and lead us to new lows. But neither has happened just yet. So price action for now may respect the ranges that are in play—both horizontal ranges and diagonal ones (channels). But it appears that price could largely could remain rangebound from a broader perspective for the coming weeks. Conclusion Traders and investors love a major directional move. It sparks adrenaline (maybe) and a combination of dreams / hopes or fears / frustration. Some traders wait eagerly at various levels to fade the move (long or short) once it has started to progress in earnest. Others who may have timed a good entry may be busy counting their profits, while trying to calm down enough to figure out a proper exit, and writing on their foreheads a reminder to "move the stop to breakeven." And still others may be sitting back patiently on the sidelines for months or years and hoping for an ideal capitulatory low after the dust has started to settle between buyers and sellers who may finally seem to have exhausted themselves. In short, the confusion and choppiness of sideways to slightly upward price action is merely the market doing price discovery between all sorts of players including long-term underwater buyers who bought above 3500 and keep hoping the price will rise just enough to make them whole (increased supply), long-term holders who are true believers in the holding (reduced supply unless emotions shake them out), short sellers (supply and potential demand when a squeeze starts), derivatives traders (supply and/or demand due to hedging flow), intraday traders, scalpers, and, let's face it, some gamblers too. In general, the market action is a device for transferring wealth from the impatient to the patient, according to one investing legend, Warren Buffett. But sometimes the patient can be the short-term trader and the impatient can be the long-term investor—because a long-term investor may lack the patience to enter or exit properly, and a short-term trader may have the patience and discipline to execute some excellent swing trades, provided risk is managed and entries and exits are well-planned, well-timed and well-executed. Minor disclaimer: This post is in no way advocating any particular investing or trading strategy. Short-term trading and long-term investing can both be either devastating or profitable (or somewhere in between those extremes) to the person engaging in it. And thanks for reading this and for your encouragement and support. ________________________________________ Author's Comment: Thank you for reviewing this post and considering its charts and analysis. The author welcomes comments, discussion and debate (respectfully presented) in the comment section. Shared charts are especially helpful to support any opposing or alternative view. This article is intended to present an unbiased, technical view of the security or tradable risk asset discussed. Please note further that this technical-analysis viewpoint is short-term in nature. This is not a trade recommendation but a technical-analysis overview and commentary with levels to watch for the near term. This technical-analysis viewpoint could change at a moment's notice should price move beyond a level of invalidation. Further, proper risk-management techniques are vital to trading success. And countertrend or mean-reversion trading, e.g., trading a rally in a bear market, is lower probability and is tricky and challenging even for the most experienced traders. DISCLAIMER: This post contains commentary published solely for educational and informational purposes. This post's content (and any content available through links in this post) and its views do not constitute financial advice or an investment or trading recommendation, and they do not account for readers' personal financial circumstances, or their investing or trading objectives, time frame, and risk tolerance. Readers should perform their own due diligence, and consult a qualified financial adviser or other investment / financial professional before entering any trade, investment or other transaction.It's hard to say yet before the week has already begun, but it looks like price is trying to spend some quality time with the down trendline from the April 16, 2023 high. If the breakout occurs, first it will be important to see whether the breakout is a trap and fails, or whether it passes on a retest. If it confirms the breakout with a successful retest, then the smaller-degree bull flag remains in play and the upside target may be achieved.No breakout yet as of this update. As discussed above, the idea is for continued sideways to slightly lower (perhaps) consolidation within this parallel channel until such time as a breakout or breakdown occurs.ETH is finding resistance at the upper edge of the downward sloping channel, i.e., the unconfirmed bull-flag pattern that lies nested within a longer-term bear flag. Here is an updated view of this chart: ETH also lies between all the longer-term anchored VWAPs discussed in the original post. Updated chart below: Note also that price is right at the upper bound of one of the triangles (on a linear chart). A decisive close above that may imply a flag-channel breakout as well which could lead to the conditional targets discussed above (upper edge of longer-term bear-flag channel, as well as measured move and Fibonacci 1.272 targets).On a 4-hour chart, it appears that the breakout occurred with a successful retest of the downward trendline (the bull-flag channel's upper bound). The next upside target logically is the VWAP anchored to the all-time high. This falls around $2037 currently.One way to gauge the continued validity / strength of the upward move is to focus on the gold uptrend line and channel from mid-June 2023 lows. It was this uptrend that propelled price through the upper boundary of the bull-flag channel shown in the main post above. And the VWAP anchored to recent swing lows is also a somewhat more flexible way to consider the short-term uptrend. Note that RSI is also pushing to a new high today relative to the prior RSI high. The immediately prior RSI high. So with RSI trending upward, this has become the bulls game to lose (in the short-term at least). Don't forget that this entire pattern appears to be nested within a larger bearish pattern.July 5 update: ETHUSD appears to be testing support at multiple trendlines at once this week.The pullback was deeper than the gold uptrend line would have suggested. But so far, the pullback has held critical support identified in the July 3 update—the VWAP anchored to the recent swing low on June 15. ETH saw a failed breakdown below this VWAP only to recover it, which can be a factor that support the short-term bullish case. If this recovery of this VWAP fails, however, this negates the short-term bullish case in favor of short-term bearish with price continuing in the downward sloping channel. If price holds above it, the breakout can still be in play. Please note that the gold uptrend line has been adjusted to account for this recent pullback. The pullback this week fell slightly below the original trendline (by about $75.00). This can happen in the early stages of any move, where initial trendlines get invalidated. Sometimes, the initial trendline is invalidated because the anticipated move / breakout fails. This is why we manage risk. But sometimes the initial trendline can be invalidated even if the move ultimately succeeds. Specifically, even a move that succeeds may invalidate the first (steeper) trendlines in favor of forming more sustainable (less steep) slopes, and such shakeouts can run stops and test / annihilate early positions. This is why it helps to have a secondary short-term gauge for a move's continued viability such as a VWAP, moving average, Fibonacci proportion, expected-move estimate based on IV, or something else.Price is arriving today at the anchored VWAP from the all-time high (red line below in updated chart). The main post on June 24 discussed this VWAP as being important (at the time, it showed a value of $2038). This ATH-anchored VWAP is now at $2033, a few points lower. On June 3, SquishTrade mentioned that a logical target after a breakout above the channel would be the ATH-anchored VWAP.The breakout from the bull-flag channel (downward sloping blue-purple lines) at first failed and fell back below this channel's upper bound. This is the channel from the mid-April 2023 highs. The updates on July 3-7, 2023, showed critical support for any viable uptrend (and continued breakout) as being the VWAP from the mid-June 2023 low. So the anchored VWAP from the mid-June 2023 low held firm as support for the recent pullback this month, and the VWAP from the mid-April 2023 low held support as well. This increased the chances of a secondary rally and breakout above the downward sloping bull-flag channel. But now the anchored VWAP from ETH's all-time high remains a point that has to be overcome for further progress upward. Please note the discussion in the main post about prior weekly tests of this ATH-anchored VWAP and how they have all failed with two-bar patterns (weekly bars). But the most recent failure did not push price significantly downward either, and prices have held trend support since the June 2022 lows last year.My technical notes for July 17, 2023: Today, here and now, several reasons have arisen to question the viability of breakout from the smaller bull-flag channel. 1. The apparent breakout from the short-term bull flag seems to be unfolding in fits and starts—sporadic and intermittent bursts higher followed by deep retraces. This sporadic and choppy action, combined with the continuing decline in volume on the weekly chart, suggests that the larger bear-flag channel controls the smaller bull-flag channel. So the longer-term bear flag perhaps dominates the overall price action despite the existence of an apparent bull-flag channel breakout. In other words, the unreliable and choppy price action post breakout could be explained by the bull-flag channel’s position as nested within a larger bear-flag channel, and the larger bear-flag channel (see primary chart above) is consolidative / corrective despite moving higher: consolidative price action is more choppy, less trendlike, and more unpredictable than trendlike action. 2. Significant failure and reaction lower at the all-time-high anchored VWAP (red), which SquishTrade had mentioned as the initial logical target for a breakout. 3. ETH seems to be taking a bit too long to make a typical trendlike move higher following the apparent smaller bull-flag breakout. Yet ETH has held the anchored VWAP from the June 15, 2023, low. 4. ETH appears to be testing important support levels shown in the chart below. Note the confluence of support being tested today: (1) Fibonacci level (yellow); (2) the downward trendline that forms the upper bound of the bull-flag channel (purple); (3) anchored VWAP from June 15, 2023. See yellow box in chart below: 4. At what point should one conclude price has fallen back within the scope of the downward-sloping bull-flag channel? —Price falls below the June 15, 2023, anchored VWAP —Price falls and holds below the downtrend line from mid-April 2023 that forms the upper bound of the bull-flag channelPRIOR ANALYSIS SUMMARIZED On June 24, the main post reviewed the consolidative nature of ETH’s price action since the June 2022 low. The analysis stated that ETH’s trend was largely sideways with a modest incline—and that this sideways to slightly upward price action appeared *consolidative* of the preceding 2022 decline. Despite a +130% move off the June 2022 lows, and another 99% move higher from the November 2022 lows, the chop and major retracements revealed that the price action was likely consolidative of the sharp and trending bear-market decline that came in 1H 2022. This is visible when looking at a higher-time frame chart such as the weekly primary chart that may be refreshed at the top of this post. At the larger / higher degree of trend, SquishTrade discussed major VWAPs from the June 2022 low and ETH’s all-time high—those VWAPs were largely sideways with price contained between them. This confirmed the consolidative nature of the price action since the 2022 lows occurred. A few triangle patterns were also shown on log and linear charts (triangle patterns also represented this larger degree consolidation). And an unconfirmed bear-flag channel—a > 1-year uptrend line that together with its return line creates a parallel channel, was noted. This modest uptrend from the June 2022 low presented the potential for prices to remain supported. In this context of consolidation, the post noted that “supported” meant that price action would remain consolidative / sideways and not crashing unless the uptrend broke. Nested within the 1-year bear flag at the larger degree of trend was a shorter-term bull-flag (a downward-sloping channel). This was tracked in the updates for a few weeks as price appeared to be breaking above it. But the breakout appeared quite weak and never rose past $2027. SquishTrade questioned the viability of this breakout on July 17. Squish described the problem with price action as follows (quotation in italics): "Today, here and now, several reasons have arisen to question the viability of breakout from the smaller bull-flag channel. 1. The apparent breakout from the short-term bull flag seems to be unfolding in fits and starts—sporadic and intermittent bursts higher followed by deep retraces. This sporadic and choppy action, combined with the continuing decline in volume on the weekly chart, suggests that the larger bear-flag channel controls the smaller bull-flag channel. So the longer-term bear flag perhaps dominates the overall price action despite the existence of an apparent bull-flag channel breakout. In other words, the unreliable and choppy price action post-breakout could be explained by the bull-flag channel’s position as nested within a larger bear-flag channel, and the larger bear-flag channel (see primary chart above) is consolidative / corrective despite moving higher: consolidative price action is more choppy, less trendlike, and more unpredictable than trendlike action. 2. Significant failure and reaction lower at the all-time-high anchored VWAP (red), which SquishTrade had mentioned as the initial logical target for a breakout. 3. ETH seems to be taking a bit too long to make a typical trend-like move higher following the apparent smaller bull-flag breakout. Yet ETH has held the anchored VWAP from the June 15, 2023, low. . . . . 5. At what point should one conclude price has fallen back within the scope of the downward-sloping bull-flag channel? —Price falls below the June 15, 2023, anchored VWAP —Price falls and holds below the downtrend line from mid-April 2023 that forms the upper bound of the bull-flag channel On July 24, one week later, price decisively fell below the June 15 low VWAP. After a retest or two, price continued to show weakness below this June 15 anchored VWAP. In short, price failed in its breakout of the bull-flag channel. In this regard, SquishTrade has so far been incorrect in the analysis that the breakout of the smaller (nested) channel would lead to the top of the bear-flag channel. But the bear-flag channel with a modest uptrend from June 2022 lows remains valid and intact. It also provides a good level to watch when and if it breaks to the upside or downside. In any case, for now, price remains controlled by and contained within the larger-degree consolidation represented by the unconfirmed bear-flag channel.UPDATED CHARTS Here are some updated charts. 1. Despite the major move downward this week, price has held (so far) between the all-time high anchored VWAP (green) and the June 2022 anchored VWAP (magenta): The June 2022 VWAP should be watched closely if the selling accelerates. A break and hold below on a daily / weekly close may suggest the consolidation being finished and a new downtrend leg starting. But that has *not* happened just yet as of this update. 2. Fibonacci levels coincide with the June 2022 VWAP (magenta) as the next levels of support if selling continues. This is emphasized with a blue rectangle on the next chart. The levels to watch (for continued viability of the uptrend since June 2022) = $1450-$1525.A couple months ago in August 2023, SquishTrade discussed ETH's confluence of support in the $1450-$1525 zone. This zone comprised a confluence of levels: (1) the upward trendline from June 2022 lows (represented by an uptrend line / parallel channel); (2) a VWAP anchored to the June 2022 bear-market low, and (3) several retracement levels shown in the August 2023 update as well. Since the August 2023 update, ETH has done a good job of holding above the anchored VWAP from the 2022 bear-market low. It has also held above the 50% retracement level shown in green below, which lies at $1510. Interestingly, the lows over the past 5 months of price weakness came in just a few points above this 50% retracement level—the October 2023 low reached $1520. Now, ETH appears to be reaching the top of the bull-flag channel—remember this bull-flag lies within an apparent larger-degree bear-flag consolidation, and this larger dominating force of bear-flag consolidation has helped explain the choppiness and unpredictability that has dominated ETH's price action since June 2022. Here is an updated chart showing the VWAP anchored to ETH's June 2022 lows along with ETH's uptrend channel (yellow) from June 2022 lows (an apparent but unconfirmed bear-flag consolidation). The light blue downtrend channel is the bull-flag channel that has guided the choppy, whipsawing price action since April 2022 highs. Further, the last chart update below shows ETH's 50% retracement level coming in at $1510 as discussed above.Furthermore, ETH longs have their work cut out for them. A bullish view into year end 2023 and into the new year requires some key levels to overcome. The most immediate level to beat is $1830 (green retracement level shown below). The next level is $1903 and the downtrend line from April 2023 highs (represented as a bull-flag / parallel channel in this post's charts). If those to levels can be overcome decisively, bullish traders may reasonably consider the measured move from June 2022 lows, which comes in at $2200-$2573 (depending on whether logarithmically charted or linearly charted). Afterwards is the upper edge of the uptrend channel from June 2023 lows around $2700 in January 2023.

SquishTrade

Cost-Benefit Analysis of Looking outside the Scope of Trend

A Cost-Benefit Analysis of Looking outside the Scope of Trend: To Peek or Not to Peek “The trend is your friend until the end when it bends.” - Ed Seykota Trend analysis lies at the core of technical analysis. Modern technical analysis derived from Dow Theory. In turn, Dow Theory emphasized the nature and importance of trends and their constituent parts and degrees. Many may recall Dow’s analogy of different trend degrees: the tide (primary trend), waves (secondary trend), and ripples on the waves (minor / short-term trend). Technical analysis includes many other concepts within its scope. But within technical analysis broadly, the primary focus remains the trend structure. Before considering trends, it may help to discuss the distinction broadly between technical analysis and fundamental analysis. A. Technical Analysis versus Fundamental Analysis Top traders and market experts have taken each side in the debate over whether technical or fundamental analysis has the greatest efficacy. Some have straddled the line, preferring a combination of the two. Some consider technical analysis to be not only superior but also relatively straightforward and efficient compared to other types of analysis, such as fundamental analysis or positioning analysis.FN1 Positioning analysis is beyond the scope of this post and is briefly explained in the first footnote. Jim Rogers, a famous investor who managed a reportedly very successful fund with George Soros in the 1970s, and who had had many accurate forecasts, expressed strong disdain for technical analysis—he once told Jack Schwager, “I haven’t met a rich technician.” But some of the greatest traders and market experts stand on the other side of this debate. For example, Ed Seykota is a trader of great renown included in Schwager’s 1993 Market Wizards: Interviews with Top Traders. Seykota chose the technical-analysis camp, giving the most weight to trends, chart patterns and good entries and exits. He once described markets in a way that evokes Charles Dow’s wave analogy: If you want to know everything about the market, go to the beach. Push and pull your hands with the waves. Some are bigger waves, some are smaller. But if you try to push the wave out when its coming in, it’ll never happen. The market is always right. A former portfolio manager for Fidelity Management who founded several other research and investment firms, David Lundgren, described how he came to follow the principles of technical analysis even though he still expressed great value for fundamental analysis. From an interview included in a 2021 Technical Analysis of Stocks and Commodities magazine, Lundgren shared some of his experiences and insights on this topic. In his view, fundamentals can matter significantly over the long term especially as to stocks. But Lundgren’s most outstanding remarks in this interview distinguished between these two conceptual approaches to financial markets. He aptly characterized fundamental analysis as being based on the view that the “market is wrong.” In other words, the valuations drawn from a publicly traded company’s financial statements (e.g., P/E ratio, enterprise value, book value) assume the market is “overestimating or underestimating value” and that the price should be above / below the current market price. By contrast, he said technical analysis assumes the contrary view that the market is actually right in its current price and price trend. The critical distinction between technical analysis and fundamental analysis boils down to ego, according to Lundgren, because pure technical analysis “accepts the verdict of the market” whereas pure fundamental analysis “involves hundreds of hours developing an opinion of what is attractive and often [conflicts] with the verdict of the market.” Much ink has and will be spilled on whether price discounts everything, and if so, how fast and efficiently (Charles Dow Theory). In any case, fundamental, technical and positioning modes of analysis are not mutually exclusive. B. Whether to Consider Data outside the Confines of Trend Since last year’s October 2022 lows in the S&P 500 (SPX) and other major US indices, the current equity market uptrend has been challenging and bewildering to many investors, traders and analysts. It has been especially difficult to comprehend for those who are keenly aware of the broader financial and macroeconomic environment, which includes purportedly tight monetary policy and quantitative tightening (reducing Treasury securities off the Fed’s balance sheet) as well as stubborn core inflation. Such an environment broadly speaking remains unfavorable to equities for the most part.FN2 But trends do not always move in the most sensible direction, and they do not always align consistently with the macroeconomic evidence. Sentiment or even positioning, discussed briefly in the first footnote, can affect the trend even when it may run counter to the macroeconomic evidence. And trends can stretch into an overbought or oversold condition longer than anyone expects, a principle captured by the old aphorism, attributed to John Maynard Keynes, that “markets can remain irrational longer than you can remain solvent.” Exhaustion doesn’t require a 180-degree turn but often appears more like a process, especially at market tops given the long-only nature of most equity capital. Pure trend followers, who supposedly consider only the technical trend-based evidence, may not care whether the trend makes sense. Indeed, they place their stops and align their trades / investments in accordance with one of many trend-based strategies. And this narrowed focus may be very helpful and exceedingly profitable at times. A recent example is the Nasdaq 100 (QQQ), or even some large or mega-cap tech names like AAPL, MSFT, META, and NVDA. These indices and securities could have rewarded narrowly focused trend-followers quite well on daily and weekly time frames over the past eight months, especially if discipline was used to enter positions at major uptrend supports with stops moved to breakeven or higher along the way. Such trend traders and investors may be busily counting their profits rather than being distracted with inverted yield curves and FOMC policy statements. The question becomes whether one may look outside the trend (or technical analysis generally). This issue likely generates pages of academic argument and hours of financial media debates between experts. And it may be something for all traders to ponder for a bit. Given how much of an influence positioning has developed on equity markets over time, as well as central-bank quantitative tightening or quantitative easing, it seems important to consider data from such sources. Such data may also include trend information that affects trends in everything else. For example, trends in the price of commodities may tell us about inflation and likelihood of tighter monetary policy / interest rate hikes by a central bank. And trends in the money supply may strengthen or weaken the case for a current trend in equities. C. Cost-Benefit Analysis of Looking beyond the Trend In this author’s view, it is not necessarily foolish or improper to sneak a peek or a long thoughtful gaze, outside a rigid trend-based framework. As with everything in life and trading, costs and benefits must be weighed. The biggest drawback to going outside the confines of trend is the tendency of many traders to try to consider far too much. Our brains are only capable of processing so much at a given time. Focusing on too much data can cause dilute confidence, weaken resolve, and obfuscate trends. In addition, by the time a trader considers a macroeconomic data point, computerized systems likely have informed all the largest institutional players, or even algorithmic or high-frequency traders, who acted on it before you even had a chance to review its implications. And the market’s reaction to non-technical data points is not always intuitive. But if one can manage understanding additional data outside the trend/price framework, one might find benefit in learning and following data on yield curves, bond-market dynamics, Fed Funds rates, macroeconomic data, inflationary measures, and volatility gauges can inform one’s outlook in useful ways. The key here is to avoid repeatedly (and blindly) fighting the trend in price—even if one fights that trend with some of the most rational, reasonable and persuasive arguments based on overwhelming macroeconomic, volatility, sentiment, positioning, or other such evidence as to why price should be going the opposite way. In short, this is the important general rule for trend-based systems—make the trend your friend until the end when it bends.FN3 D. Practical Application and Hypotheticals Just because one should make friends with the trend does not warrant chasing extended trends (see FN3), unless the trader or investor has developed particular expertise in momentum trading, and even then, caution is greatly warranted. Every trend has its proper entries for the time frame involved. Uptrends necessarily require countertrend retracements to support whether defined as an anchored VWAP, key moving average, Fibonacci retracement, upward trendline, or standard-deviation based measures such as linear regression or Bollinger Bands. Technically, this is not peeking outside the trend, but rather it merely considers evidence of trend exhaustion and the likelihood of mean reversion. Further, a trend-based framework should in fact include considering higher time frame trends such as a monthly chart where each price bar represents one month of price data. One of this author’s collaborators, spy_master , has performed some excellent trend-based analysis on timeframes as high as monthly, quarterly (even yearly bars at times). It is quite common, moreover, for higher-degree trends to move in the opposite direction as lower-degree trends, such as during a monthly or quarterly uptrend experiencing a corrective retracement to trend support that lasts for days or weeks. Or the hourly trend can move against the daily / weekly trend, frequently does so whenever a countertrend retracement to trend support occurs. Can one technically “fight the trend” merely by preferring a higher degree time-frame trend when it conflicts with a shorter one? The answer depends on one’s time frame, risk tolerance, position size, and rationale. In addition, trends involving a particular stock, index, or other security can be evaluated based on their relative strength, i.e., as a ratio of the subject stock, index or security to another stock, index, security or data series. The S&P 500 can be compared to the Nasdaq 100 or 10-year Treasures. Or ETHUSD can be charted as a ratio to another cryptocurrency. This author would argue that such metrics can provide useful trend-based insights even though they incorporate data that is technically beyond the scope of trend. Below are a couple such relative-strength charts that arguably fall within trend-analysis despite relying on data that would normally be considered outside of a price trend's scope: Example 1 shows this author's relative strength chart of AAPL to XAUUSD (Gold). This is a very long-term chart showing the outperformance trend in AAPL over two decades to the precious medal and commodity Gold. Example 2 shows spy_master 's relative-strength chart of NVDA , the AI-tech stock into which everyone's distant relatives are now inquiring after its meteoric rise from 2022 bear-market depths. The chart is a relative-strength chart of the ratio of NVDA to the 10-Year Treasury note, which aptly shows how overvalued NVDA is relative to a risk-free asset. It appears far too extended above the risk-free asset in terms of standard deviation on a linear regression-based model shown here. (Note that yields and bonds move inversely, so where an asset outperforms a risk-free bond, it means that the asset is extended given the level of yields produced by that bond.) Credit: SPY_Master (used with permission) To conclude, consider the following hypothetical scenarios as a thought experiment. Assume a stock has a monthly or quarterly chart that is extended multiple deviations above the mean (or multiple deviations as a ratio of its price to the money supply). NVDA presents a good case study for these concepts. Scenario A: A person entered the position at $290 and took profits on this stock at $405, preferring to exercise caution and avoid this stock as a long-term investment. Scenario B: A hedge fund with a 150-page report of deep research on NVDA and the macroeconomic backdrop has a 10-year time horizon and begins scaling into a short position to anticipate a mean reversion at the higher degrees of trend (monthly, quarterly time frames). The hedge fund will add one quarter at $450, another quarter position at $500, and the final two quarters between $500 and $600 if reached. Should either scenario be deemed fighting the trend? Is either scenario ill-advised use of capital? Any answers are welcome in the comments provided respectful towards others. FN1 This footnote helps explain some basics of fundamental and positioning analysis. Beyond this brief explanation, this article will defer to other educational experts for a more thorough explanation of these three modes of financial analysis. Fundamental analysis for equity indices like SPX or NDX considers macroeconomic data and metrics that focus on an economy’s growth (e.g., GDP), price-stability / inflation (CPI, PCE, PPI), consumption, real estate, money supply, central-bank rate policies, central-bank QE or QT, trade deficits, and more. Fundamental analysis as to individual stocks involves the use of financial data such as revenue, earnings per share, cost of goods sold, capital expenditures, and other data available from a public company’s certified financial statements, as well as financial ratios relying on such data, e.g., earnings per share (EPS), price-to-earnings (P/E) ratios, price-to-sales ratios (P/S) and liquidity ratios (current ratio). In the US and other major economies, securities rules mandate that companies file full disclosure of their financial health, certified by CEOs and CFOs, in annual reports (10-K and quarterly reports (10-Q) on an ongoing basis. Positioning analysis looks at a complex array of data that covers institutional market positioning and order flows for stocks, options, indices, commodities and futures. It also looks at increasingly important dealer hedging flows (volume and open interest) in options markets and the effect of implied volatility and time on such flows. It can include such insights as net positioning on each side of a given futures market or index by hedgers and speculators. This is an area where expert commentary is helpful to learn even the basics. FN2 Yet the central-bank and US Treasury actions behind the scenes may have masked, or even partially or wholly offset, tight Fed interest rate and monetary policy at times during the first half of 2023. For example, many financial publications and analysts discussed the US Treasury’s accounting maneuvers intended to prolong its borrowing authority in light of the debt-ceiling standoff. Commentary also noted that such maneuvering, draining the TGA account (the US Treasury’s “checking account” held at the Federal Reserve), injected money / liquidity into the financial system, which likely muted Fed’s efforts to tighten policy in the short-term while those actions were ongoing. FN3 But as is often the case with a general rule, the exceptions can dilute the rule somewhat. One prominent exception is mean-reversion analysis / trading systems. In addition, some traders and institutions are trend-reversal traders—a high risk, high reward type approach that requires immaculate risk management, timing, precision and patience, often scaling into and out of massive positions that cannot be acquired or unloaded in a period of days.

SquishTrade

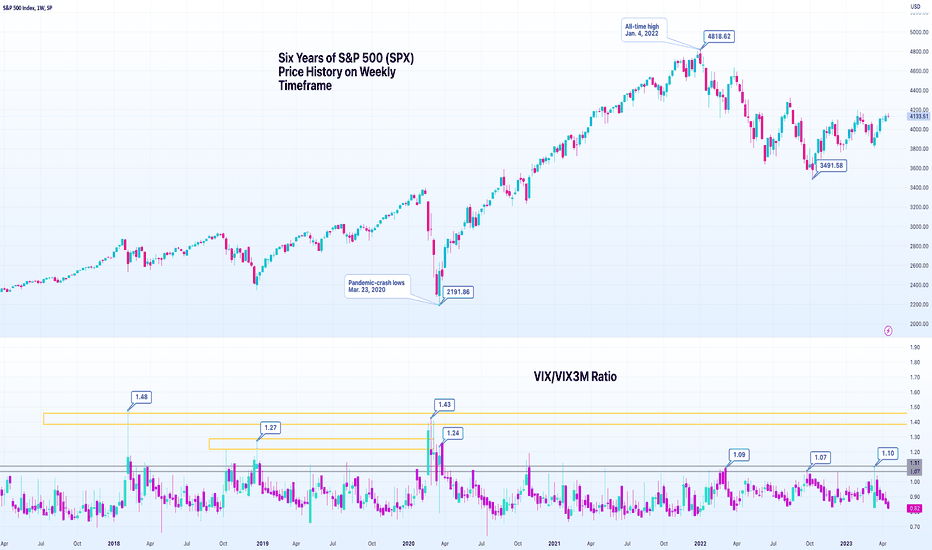

VIX/VIX3M: Tricks for Reading the VIX Part II

PRIMARY CHART: S&P 500 (SPX) with VIX/VIX3M ratio in subgraph on a weekly time frame Tricks for Reading the VIX Part I SquishTrade's original 2022 article on VIX entitled "Tricks for Reading the VIX" covered the basic concepts of the CBOE's Volatility Index (VIX) to aid in understanding and interpreting VIX and its behavior relative to the S&P 500 ( SPX ). It also explained generally how VIX values are derived, reviewed a few historical examples, and identified the historical mean (20 VIX) as well as some outliers. Furthermore, the original piece delved into the usual inverse relationship between VIX and SPX. But in its later sections, it explained how divergences from this usual inverse relationship between VIX and SPX may distinguish lasting market bottoms from interim trading lows. If interested, the following link provides the original article on VIX. A couple of points from this original article on VIX may be beneficial to readers who are less familiar with VIX. VIX is a measure of implied volatility for SPX derived from the pricing of a wide range of options prices with approximately 30 days to expiration. Specifically, only SPX options with more than 23 days and less than 37 days to expiration are included. CBOE introduced the VIX in 1993 to measure the options market's expectation of implied volatility from at-the-money SPX index options (where strikes of the options are at or very close to where the underlying index price is trading). But ten years later (2003), CBOE updated the VIX formula to track not only at-the-money options, but a wide range of SPX options focusing now on out-of-the-money strikes. CBOE's website contains a helpful FAQ on VIX here . A relevant excerpt with more detail on how VIX is calculated is available in a footnote (FN 1) at the end of this post. The last two concepts for this introduction are important. SPX implied volatility, which is what VIX is intended to measure, and realized volatility should be distinguished as they are not the same. And VIX index values tend toward mean-reversion in the long term rather than trending action. But trends within VIX can nevertheless be identified within the broader context of its mean-reverting character. SPY_Master has an excellent chart covering a recent VIX trend shown as Supplementary Chart A: Supplementary Chart A tradingview.com/x/TD6QqHDJ. VIX/VIX3M: Tricks for Reading the VIX Part II In this sequel to the original post, SquishTrade will cover the VIX/VIX3M ratio. To understand this ratio, it is important to understand basic concepts about VIX, its interpretation, and its inverse relationship as well as excepts to that relationship, which topics are covered in the prior article or elsewhere on trustworthy financial websites including CBOE's. VIX3M Basics Furthermore, VIX3M is vital to understanding the VIX/VIX3M ratio. VIX3M is essentially a 3-month forward implied volatility index for SPX. CBOE's brief description of VIX3M index follows: "The Cboe 3-Month Volatility IndexSM (VIX3M) is designed to be a constant measure of 3-month implied volatility of the S&P 500® (SPX) Index options. (On September 18, 2017 the ticker symbol for the Cboe 3-Month Volatility Index was changed from “VXV” to “VIX3M”).The VIX3M Index has tended to be less volatile than the Cboe Volatility Index® (VIX®), which measures one-month implied volatility. Using the VIX3M and VIX indexes together provides useful insight into the term structure of S&P 500 (SPX) option implied volatility." The term-structure of implied volatility (IV) means the relationship, or comparison, between different implied-volatility measures based on different terms (time periods) for measuring implied volatility such as a one-month period, three-month period, six-month period, or one-year period. Term structure can be also understood by remembering that this term is used to describe the yield curve, varying interest rates on risk-free government bonds (same type of security) with different maturities ranging from short term to long term. In short, the ratio of VIX/VIX3M allows insight into the shorter end of the IV term structure by allowing investors and traders to see both the 30-day (one-month) and the 90-day (three-month) outlook for expected volatility for SPX based on its index options premiums. VIX and VIX3M Comparison VIX3M and VIX can be distinguished based on the time frame as discussed in the prior paragraphs. One is a constant measure of approximately 30-day IV for SPX, and the other is a constant measure of approximately 3-month IV for SPX. VIX3M tends to have higher values than VIX. This is because VIX3M considers longer-dated option prices than VIX considers. The exception occurs at significant SPX lows, including interm trading lows both in bull-market retracements and in bear markets, and in more lasting bear-market lows. VIX tends to be more volatile than VIX3M. This is true even though VIX3M tends to have slightly higher values. The final point of comparison between VIX and VIX3M is that two indices are highly correlated as one might expect. This can be seen from placing them both on a chart together. Try placing them both on a chart together in TradingView, which may help some visualize and remember the close relationship between VIX and VIX3M by working with the symbols themselves. It's relatively easy to do in a couple steps. Load a chart of VIX. Then click the plus symbol next to the ticker symbol on the left upper corner of the TradingView chart screen, ad then add VIX3M to the chart. Be sure to click "New Price Scale" option when selecting VIX3M as the new symbol to be compared. VIX/VIX3M Ratio Interpretation The Primary Chart above shows the VIX/VIX3M ratio over the past six years of market history. This ratio is included in the subgraph below the SPX price chart. This chart uses a weekly time frame to ensure the data can be viewed over several years with ease. Notice how peaks in this ratio correlate to some extent with lows in SPX. Interestingly, peaks were higher in the left half of the chart between 2018 and 2020. Peaks in the current bear market have been lower relative to prior peaks in this ratio. Many peaks have been labeled on the Primary Chart for ease of reference. As discussed, VIX3M tends to have higher values than VIX. This is because VIX3M considers longer-dated option prices than VIX considers. To understand the VIX/VIX3M ratio, it helps to focus on the exception to the general rule that VIX3M tends to have higher values than VIX. The exception occurs typically when an SPX selloff causes a spike higher in VIX relative to VIX3M. Why does VIX spike higher on a relative basis, causing the ratio to rise above 1.00 / 1.10? When short-term panic occurs in markets around trading lows (or final lows as well), VIX outperforms VIX3M because VIX focuses on 30-day IV and VIX3M focuses on 90-day IV (longer-term on the IV term structure). This causes the term structure to invert briefly when VIX rises above VIX3M (which is the same as VIX3M trading at a discount to VIX). When VIX spikes above VIX3M even briefly, it shows that the market expects IV farther out on the term structure at three months to be lower than current implied volatility levels. In plain English, this means the market expects volatility to fall in several months relative to current 30-day forward levels (based on SPX options prices 23 to 37 days until expiration). And when the IV term structure normalizes as it always does after an inversion, meaning that short-term vol is lower than longer-term vol generally, this means that VIX has to fall relative to VIX3M. And remember that when VIX falls, SPX rises given the usual inverse relationship between the two. Don't forget that exceptions to this usual inverse relationship occur when VIX and SPX move in tandem, and such aberrations in the normal VIX-SPX relationship are crucial to notice as discussed in the original 2022 article on VIX. Finally, here is a chart showing a close-up view of the bear market starting in January 2022 with VIX/VIX3M shown simultaneously. The highs in this ratio were lower than prior highs at market lows over the prior decade or two. Highs have been approximately 1.05 to 1.11. Does this mean vol sellers are more opportunistic and effective? Or does it mean that we haven't seen a capitulatory low? Either way, it helps to see the current bear market levels. Enjoy! Supplementary Chart B Please see footnote 2 (FN 2) for this section on interpreting VIX/VIX3M. FOOTNOTES FN 1 Note that the formula is complicated and most likely accessible only to those still in higher-level math concentrations in their education, or those working continuously in a math field. The rest of us who have seen a few years pass since our math education must rely on the detailed verbal explanation of the formula. The formula, moreover, is unnecessary to reading and interpreting VIX values, trends, and mean reversion. CBOE's FAQ on VIX, linked above, contains the following helpful and detailed information about how the VIX Index is calculated: "Cboe Options Exchange® (Cboe Options®) calculates the VIX Index using standard SPX options and weekly SPX options that are listed for trading on Cboe Options. Standard SPX options expire on the third Friday of each month and weekly SPX options expire on all other Fridays. Only SPX options with Friday expirations are used to calculate the VIX Index.* Only SPX options with more than 23 days and less than 37 days to the Friday SPX expiration are used to calculate the VIX Index. These SPX options are then weighted to yield a constant maturity 30-day measure of the expected volatility of the S&P 500 Index. Cboe Options lists SPX options that expire on days other than Fridays. Non-Friday SPX expirations are not used to calculate the VIX Index. Intraday VIX Index values are based on snapshots of SPX option bid/ask quotes every 15 seconds and are intended to provide an indication of the fair market price of expected volatility at particular points in time. As such, these VIX Index values are often referred to as "indicative" or "spot" values. Cboe Options currently calculates VIX Index spot values between 3:15 a.m. ET and 9:15 a.m. ET (Cboe GTH session), and between 9:30 a.m. ET and 4:15 p.m. ET (Cboe RTH session) according to the VIX Index formula that is set forth in the White Paper." FN 2 The source for some of the key concepts in this section was a January 2018 article on CBOE's website blog on the VIX / Trader Talk, and the article referenced was "Vol 411 Follow Up: More on the VIX3M / VIX Ratio." This article appears to no longer be available. ________________________________________ Author's Comment: Thank you for reviewing this post and considering its charts and analysis. The author welcomes comments, discussion and debate (respectfully presented) in the comment section. Shared charts are especially helpful to support any opposing or alternative view. This article is intended to present an unbiased, technical view of the security or tradable risk asset discussed. Please note further that this technical-analysis viewpoint is short-term in nature. This is not a trade recommendation but a technical-analysis overview and commentary with levels to watch for the near term. This technical-analysis viewpoint could change at a moment's notice should price move beyond a level of invalidation. Further, proper risk-management techniques are vital to trading success. And countertrend or mean-reversion trading, e.g., trading a rally in a bear market, is lower probability and is tricky and challenging even for the most experienced traders. DISCLAIMER: This post contains commentary published solely for educational and informational purposes. This post's content (and any content available through links in this post) and its views do not constitute financial advice or an investment or trading recommendation, and they do not account for readers' personal financial circumstances, or their investing or trading objectives, time frame, and risk tolerance. Readers should perform their own due diligence, and consult a qualified financial adviser or other investment / financial professional before entering any trade, investment or other transaction. Thank you for reading. If this post added clarity or prompted additional thoughts on the technicals of SPY, please comment below!spy_master raised a very good point in the comments about the term backwardation. First, backwardation and contango are technically terms used in the futures context, and this article represents indices. Nevertheless, the concept is the same. When near term vol rises above longer term vol, this is inversion of the normal term structure, and it's called backwardation. The futures curve for VIX becomes "backwardated" or "in backwardation" when when near term contracts rise above longer term contracts. This illustration provided by spy_master in the comments is instructive: Note VX refers to a Vix futures contract. So when VIX rises above VIX3M (so that the ratio VIX/VIX3M rises above 1.0), this is analogous to at least a portion of the futures curve being in backwardation. One key point here is that an inversion in VIX and VIX3M represented by VIX/VIX3M rising above 1.0 does not necessarily mean the entire VX futures curve is in backwardation. This still provides valuable information. In a bull market, a brief pop above 1.10 or 1.20 might signal a near term end to a pullback—which is signaled without the need for a full VX futures curve inversion / backwardation. But the lack of a backwardation in the entire curve is also instructive, and this is something that would require watching the VX futures curve. Please be sure to check out SPY's comments below about the lack of full backwardation at the October 2022 low, which is something that you may find important to ponder! Thanks to SPY for the post-hoc collaboration in the comments! Any other commentary, debate or disagreement is welcome as always (provided it's civil)This week has seen a swift increase in volatility coinciding with the sharp downward move in SPX / SPY and equities in general. To illustrate how short-dated vol rises much quicker and higher than longer-dated vol, notice the following performance comparisons for different vol-term lengths. Note that the comparison shows the percentage move off the recent mid-April vol lows in each vol index. The vol lows didn't necessarily land on the same day, though they were all in mid-April generally. 1. VIX9D rose 57.6% off mid-April lows 2. VIX rose +22.82% off mid-April lows 3. VIX3M rose +14.12% off 4/18/23 lows 4. VIX6M rose +11.76% off 4/18/23 lows. Those buying shorter vol tend to see a much bigger move in options premiums. Shorter dated vol may mean (in this context) shorter-term VX futures or shorter-dated VIX options or it may mean short-dated SPX or NDX puts that have much higher risk for example. This bigger move is not without higher risk that always comes with shorter-dated options, which have exploded in recent months and years, rising to nearly 40-50% of total options volume on major indices per options-hedging flows experts.Yesterday, VIX hit 1.4 year lows. The lows in VIX had not been seen at this level since November 2021. VIX also showed positive divergence using momentum indicators—in other words, as values made lower lows, momentum made higher lows (RSI in particular). Assuming TA can be applied to such a mean-reverting index, it's unsurprising to see a push higher in VIX today.VIX has been making 1.5 year lows since April this year. So it's no surprise that this ratio of VIX/VIX3M is as well. VIX/VIX3M, discussed in this educational post, is this week pushing back toward major 1.5-year support ■ shows steep contango in this segment of VIX term structure ■shows potential complacency in short-term, which *could* coincide with short to intermediate term peaks in SPX and lows in vol. Let's see what happens. And here is a chart by GammaLab , one of SquishTrade's favorite follows. This chart shows a comparison of both 1-month realized vol and 1-month IV. And it goes back far enough to shows trends in both implied volatility (IV) and realized volatility (RV). Notice how RV (green) fell hard into new lows in April 2023 reflecting SPX's choppy, tight sideways price range that lasted nearly 1.5 months from the start of April to mid-May 2023. With the big move up in SPX from early June 2023, with SPX 4448 new YTD highs last week, realized vol has risen, and IV along with it. Other analysts and technicians have been noting that the "vol up / spot up" phenomenon was starting to be seen in fixed strike vol last week. Will this upward curve at the right-hand side of the chart continue? There are reasons to think it could at least in the near term. Opinion Disclaimer : The views and opinions expressed in this update are solely those of SquishTrade and do not reflect the views or opinions of GammaLab, the source of the second chart shown in this update.

SquishTrade

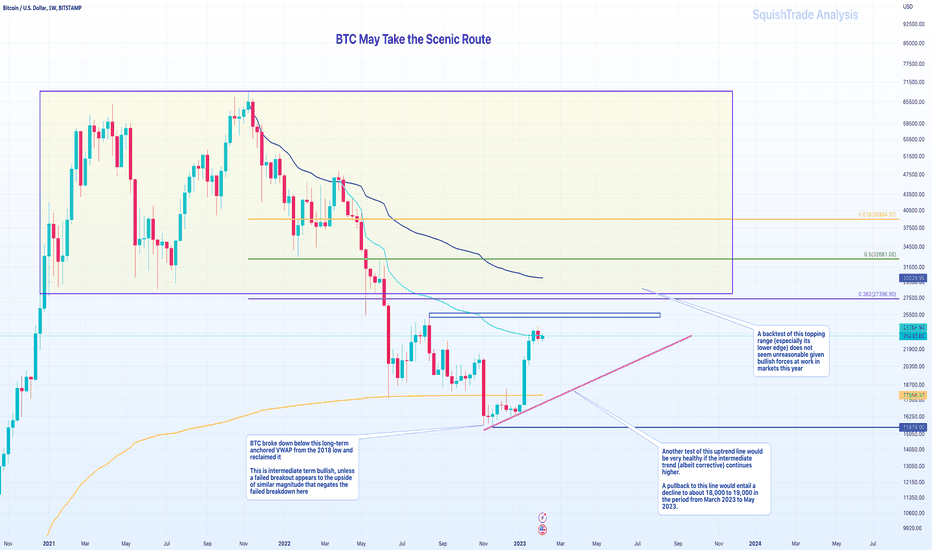

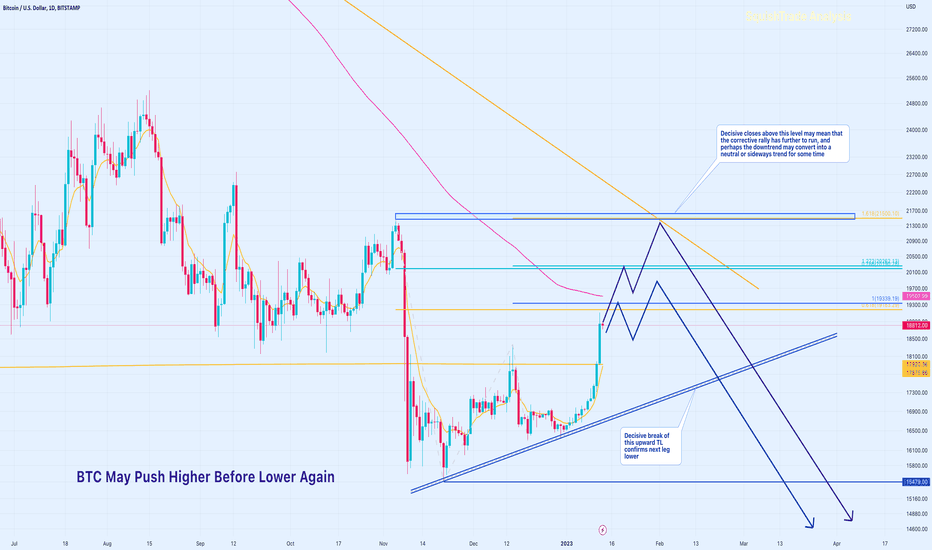

BTC May Take the Scenic Route