thunderpips

@t_thunderpips

تریدر چه نمادی را توصیه به خرید کرده؟

سابقه خرید

تخمین بازدهی ماه به ماه تریدر

پیام های تریدر

فیلتر

نوع پیام

thunderpips

Bitcoin's Wild Ride: Will It Moon or Crash and Burn?

آه ، بیت کوین - غلتکی دیجیتال که همه ما دوست داریم از آن متنفر باشیم. در حال حاضر در حال دور زدن 84000 دلار ، اما بعد چیست؟ بیایید به توپ کریستالی پیش بینی های رمزنگاری شیرجه بزنیم ، باید؟ 🔮 رویای صعودی: مشتقات لذت بخش: برخی از تحلیلگران نسبت به معیارهای مشتقات بسیار جالب توجه هستند ، و نشان می دهد که Bitcoin "آماده" برای بازپس گیری سطح 90،000 دلار در هفته های آینده است. چون چه کسی قمار خوبی را دوست ندارد؟ رئالیست های نزولی: درام صلیب مرگ: روی کلاه های خود نگه دارید! Bitcoin در حال معاشقه با "صلیب مرگ" است ، جایی که میانگین متحرک 50 روزه زیر 200 روز فرو می رود. از نظر تاریخی ، این مانند نسخه رمزنگاری یک فیلم ترسناک است - موسیقی نمایشی را تهیه کنید. سطح پشتیبانی shenanigans: اگر Bitcoin نمی تواند قدرت ماندن بالاتر از 81000 دلار را بدست آورد ، ممکن است سریعتر از آنچه می توانید بگویید "HODL" به 76000 دلار کاهش می یابد. حصار: FOMC Follies: همه نگاه ها به جلسه آینده کمیته بازار آزاد فدرال است. آیا نرخ آنها افزایش می یابد؟ آیا آنها برش می دهند؟ آیا آنها برای ناهار پیتزا سفارش می دهند؟ تصمیمات آنها می تواند Bitcoin را بر روی یک جوی یا یک شستشو ارسال کند. بنابراین ، غذای آماده چیست؟ آیا Bitcoin برای یک مأموریت ماه آماده است ، یا ما برای یک سقوط آزاد درگیر هستیم؟ مثل همیشه ، عقل خود را در مورد خود نگه دارید ، و شاید یک چتر نجات مفید باشد. 🎢🪂 اگر می شکست عمیق تر (کسی که هیچ کس به شما نمی گوید) ، نظر خود را رها کنید یا من را DM کنید. شاید من به شما اجازه می دهم در مورد بینش های واقعی. 👀🔥 سلب مسئولیت: این مشاوره مالی نیست. همیشه قبل از غواصی در پرتگاه رمزنگاری ، تحقیقات خود را انجام دهید.

thunderpips

Gold at $3,000: The Ultimate Panic Buy or Just Another Bubble?

💰 طلا در رکورد اوج قرار می گیرد - زیرا جهان در آتش است آه ، دکمه وحشت مورد علاقه بشریت. از نظر مارس 2025 ، قیمت های طلا گذشته است 3000 دلار در هر اونس بشر چرا؟ زیرا جهان نمی تواند پنج دقیقه بدون بحران برود. 🌍💥 جنگ های تجاری؟ بررسی کنید درگیری های ژئوپلیتیکی؟ بررسی کنید مبارزات ابدی بین "متخصصان" پیش بینی عذاب و ماهواره ها که فریاد می زنند "خرید شیب"؟ بررسی کنید با U. S. اقتصاد سرمایه گذاران مانند یک عکس تکیلا و عدم اطمینان جهانی در همه زمانها ، مانند یک برج تمام وقت ، مانند این آخرین قایق نجات در تایتانیک هستند. 🚢💨 🏦 بانکهای مرکزی: نگهبانان طلای نهایی اگر فکر می کنید اعتیاد به طلا دارید ، با بانک های مرکزی ملاقات کنید. این بچه ها سالانه بیش از 1000 تن متریک خریداری می کنند - به طور کلی طاق های خود را به اژدها تبدیل می کند. 🐉💰 چرا؟ از آنجا که آنها قطعاً به ارزهای فیات اعتماد دارند ... فقط کافی نیست که از سیاست های خود محافظت نکنند. 😏 چین ، هند و ترکیه در حال پیشبرد شارژ هستند ، مانند یک نسخه محدود NFT ، طلا را جمع می کنند. منطق؟ اگر همه چیز به جهنم می رود ، حداقل آنها چیزی زیبا برای دیدن دارند. 📈 "افراد باهوش" چه فکر می کنند؟ (اسپویلر: آنها موافق نیستند) بیایید بررسی کنیم که چه بانک های بزرگ می گویند - زیرا اگر یک چیز وجود دارد که بانک ها در آن عالی هستند ، با پیش بینی های آنها به طور مداوم اشتباه می کند. JP Morgan Bank Private احساس است "سازنده" درباره طلا که فقط یک روش فانتزی برای گفتن است "آه ، ما هیچ سرنخی نداریم ، اما به نظر می رسد خوب است." آنها فکر می کنند که کاهش بالقوه نرخ فدرال فدرال می تواند طلا را بالاتر ببرد. 🚀 ورک برجسته می کند چگونه بانک های مرکزی و سرمایه گذاران در سال 2024 طلا را به اوج های جدید سوار کنید. اساساً ، همه در حال اجرا هستند و در حالی که وانمود می کنند این یک "تخصیص استراتژیک" است. 🤔 آیا باید طلا بخرید یا فقط هرج و مرج را تماشا کنید؟ Pros: شما یک سنگ براق می گیرید که همه ناگهان در طی یک بحران به آن اهمیت می دهند. 🌟 منفی ها: بدون سود سهام ، بدون درآمد منفعل ، و شما اساساً امیدوار هستید که برخی از مکنده ها بیشتر از آنچه پرداخت می کنند بپردازند. 😬 طلا یک است پرچین بزرگ وقتی جهان در حال ذوب شدن است ، اما اجازه ندهید که این یک تولید کننده ثروت جادویی باشد. اگر در حال خرید هستید ، فقط مطمئن شوید که به این دلیل نیست که راننده Uber شما گفت "به ماه می رود". 🚀🌕 (نه مشاوره مالی. اما قطعاً مشاوره طعنه آمیز. 🤷♂) اگر می شکست عمیق تر (کسی که هیچ کس به شما نمی گوید) ، نظر خود را رها کنید یا من را DM کنید. شاید من به شما اجازه می دهم در مورد بینش های واقعی. 👀🔥

thunderpips

GOLD - FUNDAMENTAL ANALYSIS

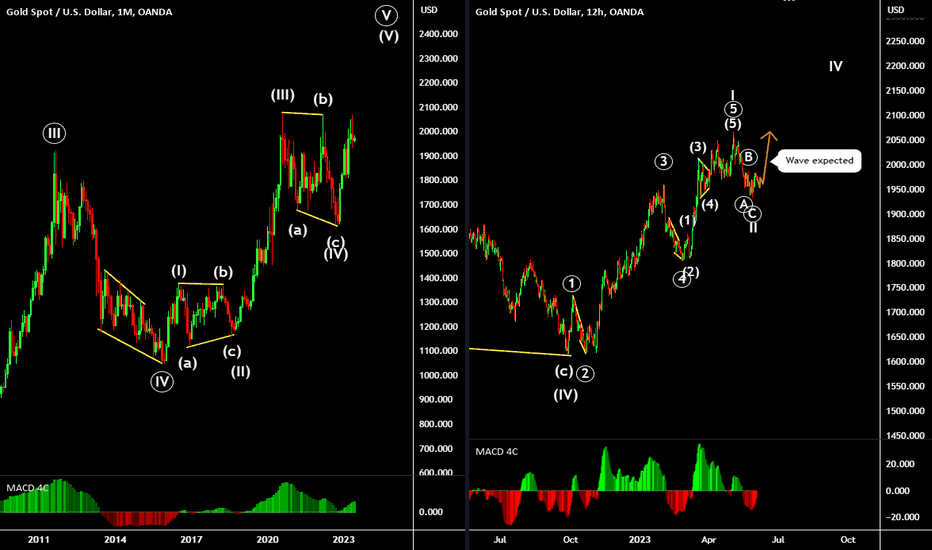

پیش بینی های قیمت طلا برای پایان سال 2023 و 2024 در ABN AMRO اصلاح شده است در یادداشت گسترده استراتژیک XAU به مشتریان ، Georgette Boele ، اقتصاددان ارشد ABN Amro هشدار داد که پیش بینی قیمت طلای 2023 و 2024 بانک را کاهش می دهد. این تحلیلگر از قیمت طلا نزدیک به اوج تمام وقت استناد می کند ، سطحی که باید سقوط کند ، ممکن است برای پنج سال دیگر دیده نشود. با کاهش سیاست های پولی فدرال رزرو ، افزایش قیمت ، صعود احتمالاً از اینجا محدود بود. قیمت طلا تاکنون در سال 2023 نامنظم بوده است. قیمت طلا سال را با یک یادداشت صعودی آغاز کرد و تا 4 ماه مه 13 درصد افزایش قیمت ها را ثبت کرد. به گفته تحلیلگر ، با این حال ، حرکت از آن زمان پرچم گذاری شده است ، و به نظر می رسد که گرانبها metal اکنون در مرحله ادغام قرار دارد. این تغییر در روند با مشاهدات بول مبنی بر اینکه سرمایه گذاران ممکن است از خرید در سطوح فعلی دریغ کنند ، به ویژه با وجود افت چشمگیر در بازار. اشاره به ماهیت ریسک پذیر سرمایه گذاران طلا ، که تمایل به اولویت بندی ثبات بلند مدت نسبت به سودهای کوتاه مدت دارند. تغییر Boele در چشم انداز فدرال رزرو وی به طور قابل توجهی پیش بینی های وی را آگاه می کند. در ابتدا ، او انتظار نداشت که در کوتاه مدت یک سرعت تهاجمی کاهش یافته باشد ، اما معتقد بود که چرخه تسکین به پایان سال 2023 آغاز می شود. با این حال ، تحولات اخیر باعث شده است که وی به تجدید نظر در این انتظارات بپردازد. بول می گوید: "هفته گذشته ، ما دیدگاه فدرال و همچنین نمای دلار آمریکا را تغییر دادیم." وی افزود: "ما اکنون انتظار داریم که رکود اقتصادی در Q4 آغاز شود و کاهش نرخ در Q1 2024 به وجود آید. ما انتظار داریم آخرین نرخ افزایش 25bp در جلسه ژوئیه فدرال رزرو و هیچ کاهش نرخ امسال باشد. ما هنوز کاهش نرخ تهاجمی را در سال 2024 پیش بینی می کنیم. اکنون در سال 2024 175 کاهش نرخ نرخ نرخ داریم." این پیش بینی نشان می دهد که اعتقاد وی مبنی بر اینکه فدرال رزرو برای تحریک اقتصاد و مبارزه با فشارهای رکود اقتصادی که انتظار می رود ظهور کند ، اقدامات ادعا را انجام می دهد. در راستای انتظارات تغییر یافته او برای فدرال رزرو ، دیدگاه بول در مورد دلار آمریکا نیز تکامل یافته است. با کاهش کمتر نرخ انتظار برای باقیمانده سال 2023 و تا سال 2024 ، وی دیدگاه خود را به دلار آمریکا ارتقا داده و این را به عنوان یک چرخش مثبت می داند. این تغییر نشان دهنده اعتقاد وی به مقاومت در برابر دلار آمریکا و عملکرد احتمالی آن در مواجهه با شرایط نامطلوب اقتصادی است. این تحلیلگر می گوید: "در نتیجه تغییر در دیدگاه فدرال رزرو ما ، دیدگاه خود را در مورد دلار آمریکا ارتقا داده ایم." "ما دیگر امسال کاهش نرخ برای فدرال رزرو و کاهش نرخ کل در 2023-2024 را نداریم. این برای دلار آمریکا مثبت است. دیدگاه ما تقریباً مطابق با بازار است." بول خاطرنشان می کند که انتظارات نرخ ، چه واقعی و چه اسمی ، در کنار چشم انداز دلار آمریکا ، محرک های مهم قیمت طلا هستند. در نتیجه ، چشم انداز تعدیل شده او برای فدرال رزرو و دلار آمریکا باعث شده است تا پیش بینی قیمت طلای خود را برای سال 2024 کاهش دهد. اقتصاددان می گوید: "بنابراین ما همچنین پیش بینی قیمت طلای خود را برای 2024 به 2،000 دلار در هر اونس کاهش داده ایم (از 2200 قبل از آن) که اکنون برای 2023 و 2024 پیش بینی سال 2000 را داریم." با وجود کاهش احتمالی فدرال رزرو ، به طور معمول به عنوان یک مزیت برای قیمت های طلا در نظر گرفته می شود ، Boele پتانسیل بالایی برای طلا در رابطه با دلار آمریکا می بیند. وی خاطرنشان می کند ، سرمایه گذاران در حال حاضر دارای موقعیت های طلای خالص هستند و این خطر وجود دارد که بخشی از اینها انحلال شود. "استدلال پشت این چیست؟" او می پرسد. وی می افزاید: "شروع تسکین سیاست پولی توسط FED به طور کلی برای قیمت های طلا مثبت است. اما همانطور که بازار قبلاً این موضوع را پیش بینی کرده است ، در حال حاضر در قیمت طلا منعکس شده است. بنابراین ما فکر می کنیم که صعود در قیمت های طلا در مقابل دلار آمریکا از سطح فعلی محدود است." Boele یک کلمه احتیاط را برای سرمایه گذاران ارائه می دهد. با توجه به سطح بالای قیمت طلا و خطرات بالقوه ، وی اظهار داشت که طولانی بودن ممکن است جذاب ترین موضع از منظر ریسک-پاداش نباشد.

thunderpips

GOLD FUNDAMENTAL ANALYSIS

در میان مهلت بدهی ایالات متحده ، تحولات اخیر باعث شده است که به سمت طلا به عنوان ابزاری برای پرچین خطر تبدیل شود. سرمایه گذاران از نزدیک تأثیر احتمالی توافق نامه سقف بدهی ایالات متحده و پیامدهای آن را برای هزینه های فدرال بررسی می کنند. "Ehsan Khoman ، رئیس کالاها ، ESG و تحقیقات بازارهای نوظهور در MUFG می گوید:" فیچ رتبه حاکمیت ایالات متحده را بر روی یک رادار منفی ساعت به عنوان مهلت بدهی منتقل می کند. سرمایه گذاران همچنین در حال ارزیابی تأثیر احتمالی معامله سقف بدهی ایالات متحده و چگونگی کاهش هزینه های فدرال هستند. " با توجه به شرایط خاص اقتصادی ، طلا به عنوان یک پناهگاه امیدوار کننده مورد توجه قرار می گیرد. Khoman می افزاید: "این سرمایه گذاران را به سمت طلا سوق داده بود ، به عنوان پرچین در برابر خطر." پیچیدگی محیط مالی فعلی به ویژه جذابیت طلا را تقویت کرده است. طلا در یک محیط اقتصادی چالش برانگیز بهتر است در حالی که فدرال رزرو علیرغم افزایش قیمت های تولید کننده ، عرضه پول و سپرده های بانکی ، همچنان محکم تر می شود ، طلا به عنوان یک مجری درخشان ظاهر می شود. Khoman خاطرنشان می کند: "ترکیب بی سابقه ای از فدرال رزرو هنوز هم در H1 2023 با وجود افزایش قیمت های تولید کننده ، عرضه پول و سپرده های بانکی ، به نفع طلا است." گرانبها metal سایر نمایندگان شاخص کالای بلومبرگ را به صورت سالانه پیشی گرفته است. به گفته این تحلیلگر ، احتمالاً موقعیت سودمند گلد همچنان ادامه یافت زیرا جهان فراتر از هجوم فدرال رزرو است. خومن می گوید: "گزاره ارزش طلا سازنده باقی مانده است زیرا ما در حال گذر از هجوم تغذیه هستیم زیرا ایالات متحده به نظر می رسد بدون رشد در جای دیگر ، کند می شود." این کندی اقتصادی می تواند باعث افزایش تقاضای سرمایه گذاری برای طلا شود ، که در سالهای اخیر نسبتاً خفته بوده است. بازار نوظهور بانکهای مرکزی تقاضای طلا را بالا نگه می دارند بانک های مرکزی در بازارهای نوظهور (EM) به طور فعال طلا را بدست می آورند ، روندی که تقاضا برای گرانبها را قوی نگه داشته است. این سرعت خرید توسط خطرات ژئوپلیتیکی و روند De-Dolarisation هدایت می شود. خلمن توضیح می دهد: "بانکهای مرکزی EM همچنان به خرید طلا با سرعت ادامه می دهند-روندی که انتظار داریم همچنان بر تقاضای طلا در پشت خطرات ژئوپلیتیکی بالا و روندهای غیرقانونی حاکم شود." در میان این نیروها ، مسیر قیمت طلا در حال افزایش است ، البته با سرعت بالقوه کندتر از آنچه قبلاً دیده می شد. این تحلیلگر در ادامه می گوید: "به طور کلی ، این نشان می دهد که طلا آماده است تا بالاتر برود ، اگرچه ممکن است بیشتر از ادامه سنبله کند." مدل های قیمت طلای MUFG به طور متوسط امسال 1،980 دلار در هر اونس پروژه می کند و تمایل به فراتر از این پیش بینی قیمت دارد. Khoman پیشنهاد می کند ، "مدل های قیمت طلای ما به طور متوسط امسال 1،980 دلار در هر اونس نشان می دهد که خطرات آن به صعود رسیده است." تحلیلگر طلا نتیجه می گیرد که در آب و هوای افزایش اضطراب و خطرات رکود اقتصادی ، روند نزولی بالقوه برای طلا در یک فرود نرم یا حرکات هولناک بیشتر از فدرال رزرو به طور قابل توجهی کمتر از صعود در صورت ایجاد شوک رشد است که اقتصاد ایالات متحده را به سمت رکود سوق می دهد. با این حال ، ممکن است برای طلا برای عبور از 2،100 دلار در هر آستانه اونس بدون اینکه فدرال رزرو کند برای کاهش نرخ در پاسخ به رکود اقتصادی که نیاز به محوریت حمایت از رشد دارد ، چالش برانگیز باشد.

thunderpips

GOLD FUNDAMENTAL ANALYSIS

در میان مهلت بدهی ایالات متحده ، تحولات اخیر باعث شده است که به سمت طلا به عنوان ابزاری برای پرچین خطر تبدیل شود. سرمایه گذاران از نزدیک تأثیر احتمالی توافق نامه سقف بدهی ایالات متحده و پیامدهای آن را برای هزینه های فدرال بررسی می کنند. "Ehsan Khoman ، رئیس کالاها ، ESG و تحقیقات بازارهای نوظهور در MUFG می گوید:" فیچ رتبه حاکمیت ایالات متحده را بر روی یک رادار منفی ساعت به عنوان مهلت بدهی منتقل می کند. سرمایه گذاران همچنین در حال ارزیابی تأثیر احتمالی معامله سقف بدهی ایالات متحده و چگونگی کاهش هزینه های فدرال هستند. " با توجه به شرایط خاص اقتصادی ، طلا به عنوان یک پناهگاه امیدوار کننده مورد توجه قرار می گیرد. Khoman می افزاید: "این سرمایه گذاران را به سمت طلا سوق داده بود ، به عنوان پرچین در برابر خطر." پیچیدگی محیط مالی فعلی به ویژه جذابیت طلا را تقویت کرده است. طلا در یک محیط اقتصادی چالش برانگیز بهتر است در حالی که فدرال رزرو علیرغم افزایش قیمت های تولید کننده ، عرضه پول و سپرده های بانکی ، همچنان محکم تر می شود ، طلا به عنوان یک مجری درخشان ظاهر می شود. Khoman خاطرنشان می کند: "ترکیب بی سابقه ای از فدرال رزرو هنوز هم در H1 2023 با وجود افزایش قیمت های تولید کننده ، عرضه پول و سپرده های بانکی ، به نفع طلا است." گرانبها metal سایر نمایندگان شاخص کالای بلومبرگ را به صورت سالانه پیشی گرفته است. به گفته این تحلیلگر ، احتمالاً موقعیت سودمند گلد همچنان ادامه یافت زیرا جهان فراتر از هجوم فدرال رزرو است. خومن می گوید: "گزاره ارزش طلا سازنده باقی مانده است زیرا ما در حال گذر از هجوم تغذیه هستیم زیرا ایالات متحده به نظر می رسد بدون رشد در جای دیگر ، کند می شود." این کندی اقتصادی می تواند باعث افزایش تقاضای سرمایه گذاری برای طلا شود ، که در سالهای اخیر نسبتاً خفته بوده است. بازار نوظهور بانکهای مرکزی تقاضای طلا را بالا نگه می دارند بانک های مرکزی در بازارهای نوظهور (EM) به طور فعال طلا را بدست می آورند ، روندی که تقاضا برای گرانبها را قوی نگه داشته است. این سرعت خرید توسط خطرات ژئوپلیتیکی و روند De-Dolarisation هدایت می شود. خلمن توضیح می دهد: "بانکهای مرکزی EM همچنان به خرید طلا با سرعت ادامه می دهند-روندی که انتظار داریم همچنان بر تقاضای طلا در پشت خطرات ژئوپلیتیکی بالا و روندهای غیرقانونی حاکم شود." در میان این نیروها ، مسیر قیمت طلا در حال افزایش است ، البته با سرعت بالقوه کندتر از آنچه قبلاً دیده می شد. این تحلیلگر در ادامه می گوید: "به طور کلی ، این نشان می دهد که طلا آماده است تا بالاتر برود ، اگرچه ممکن است بیشتر از ادامه سنبله کند." مدل های قیمت طلای MUFG به طور متوسط امسال 1،980 دلار در هر اونس پروژه می کند و تمایل به فراتر از این پیش بینی قیمت دارد. Khoman پیشنهاد می کند ، "مدل های قیمت طلای ما به طور متوسط امسال 1،980 دلار در هر اونس نشان می دهد که خطرات آن به صعود رسیده است." تحلیلگر طلا نتیجه می گیرد که در آب و هوای افزایش اضطراب و خطرات رکود اقتصادی ، روند نزولی بالقوه برای طلا در یک فرود نرم یا حرکات هولناک بیشتر از فدرال رزرو به طور قابل توجهی کمتر از صعود در صورت ایجاد شوک رشد است که اقتصاد ایالات متحده را به سمت رکود سوق می دهد. با این حال ، ممکن است برای طلا برای عبور از 2،100 دلار در هر آستانه اونس بدون اینکه فدرال رزرو کند برای کاهش نرخ در پاسخ به رکود اقتصادی که نیاز به محوریت حمایت از رشد دارد ، چالش برانگیز باشد.

thunderpips

GOLD FUNDAMENTAL ANALYSIS

The US dollar (USD) has staged a comeback against the Pound Sterling (GBP) and Euro (EUR) over the past few weeks, but foreign exchange analysts at MUFG still consider that medium-term depreciation is the most likely outcome. The bank considers that the US Dollar exchange rates are overvalued, especially against the Japanese Yen (JPY) and net capital flows are likely to be less supportive. It also considers that the Euro-Zone and Chinese outlooks are more favourable, especially given that gas prices have declined sharply. MUFG also expects the Fed will cut rates before the ECB while the Bank of Japan will tighten policy. Monetary policy will inevitably be a key aspect. Although the immediate debate is still surrounding the potential for further interest rate hikes, MUFG expects the debate will switch to the potential for a Federal Reserve policy reversal as the US economy deteriorates. According to the bank; “ The Fed will be cutting rates prior to the ECB. Inflation in Europe is stickier due to energy and food prices and the Fed will have much more scope to respond once economic conditions in the US weaken further from here. ” After an extended period of quantitative easing, MUFG also expects that the ECB quantitative tightening programme through bond sales will put upward pressure on longer-term yields and support the Euro. Global Growth Trends Still Favourable MUFG notes that previous forecasts of an extended UK recession have been revised away and the Euro-Zone has also been resilient. As far as China is concerned it adds; “ Recent data has disappointed, in particular on the manufacturing side of the economy, but pent-up domestic demand likely has further to run which will act as a source of global growth this year. ” Although market sentiment has been more cautious, it expects overall growth dynamics will not favour the US dollar as Asia rebounds. A related issue is the key area of energy prices. The jump in energy costs last year was a key reason why agencies such as the IMF and central banks were so negative surrounding the European economic outlook last year. Gas prices have, however, declined sharply with a slump from over 90% from the peak and close to 2-year lows. Gas storage levels are also at very high levels in historic terms ang MUFG expects storage levels will hit 100% in the summer. In this context, lower gas prices will improve the growth outlook and strengthen the trade outlook. The Bank of Japan has resisted tightening monetary policy, but MUFG notes that the economy is strengthening and inflation has increased. According to MUFG; “ we maintain that YCC has passed its sell-by-date and while it remains unclear whether price stability at 2% can be achieved, the BoJ will still move to widen the band or scrap it completely. ” The bank expects that the yen will strengthen sharply if the Bank of Japan lets yields increase which will drag the dollar lower. Negative Long-Term US Debt Dynamics The immediate focus is on the US debt ceiling and political brinkmanship ahead of early June when the US Treasury will run out of cash. These short-term dynamics are mixed for the US dollar with concerns over the economy, but potential defensive support if risk appetite deteriorates. MUFG focusses on the underlying debt dynamics and the potentially unsustainable situation. MUFG notes that the budget deficit in the first seven months of fiscal 2022/23 amounted to $928bn from $360bn the previous year. On a longer-term view, in considers the debt dynamics will be potentially negative for the US currency. De-Dollarization Hype Although MUFG considers that the de-dollarization rhetoric is rather more hype than substance, there is still the risk that long-term confidence in the dollar will decline with scope for some further increase in Euro and yuan central bank reserve holdings. MUFG also notes that there has been strong central bank gold buying and it expects this trend will continue. The bank also sees a risk that the US use of financial sanctions will discourage official players to hold reserves in the dollar due to fears over asset freezes. MUFG notes that there has been an extended period of Wall Street out-performance, but expects this trend will reverse and net capital flows will be less supportive for the US currency. It adds; “ We see a renewed drop in US equities as investors position more assertively for US recession. ” Japan’s Nikkei 225 index has posted a 32-year high and the German DAX index has hit a record high. It also sees scope for a sustained rebound in emerging-market equities after an extended period of under-performance. It adds; “ A reversal of the current period of deep EM undervaluation poses downside risks for the USD in the medium-term. ” Long-Term Peak, Dollar Overvalued MUFG notes that the dollar last year reached the highest level for over 20 years. It also notes that at the October peak the currency index was 2 standard deviations stronger than the average over the past 40 years. It adds; “ Similar extreme levels of USD overvaluation were last recorded in the early 2000’s and mid-1980’s and subsequently proved to be long-term bearish turning points for the USD. ” The bank also considers that the dollar is substantially overvalued, especially against the yen, increasing the likelihood of mean reversion.

thunderpips

BTC USD FUNDAMENTAL ANALYSIS

قیمت Bitcoin اخیراً از بازار سهام جدا شده است که در نتیجه آن حتی بحران بانکی اخیر تأثیری نزولی بر ارز دیجیتال نداشته است. اکنون با بازگشت روند "فروش در ماه مه"، این احتمال وجود دارد که BTC از مزایای بازار سهام با رشد آهسته بهره مند شود. "فروش در ماه مه" - سقوط بانک ها راه را هموار می کند در بازار سهام، با پایان ماه آوریل، یک ضرب المثل رایج در بین سرمایه گذاران زنده می شود - "در ماه می بفروش و برو. این اصل برای نشان دادن آغاز بدترین شش ماه سال برای معامله گران و سرمایه گذاران استفاده می شود. با توجه به عملکرد نسبتاً وحشتناک بازار سهام، یعنی شاخص S&P 500 (SPX)، "فروش در ماه می" پیشنهاد می کند به سادگی شش ماه آینده را نادیده بگیرید و دوباره در اکتبر بازگردید. در حالی که ممکن است مد دیگری به نظر برسد، اما از نظر تاریخی درستی این گفته ثابت شده است. بر اساس گزارشی از کارسون، به طور متوسط دوره می تا اکتبر کمترین رشد 1.7 درصدی را در مقایسه با سایر ترکیبات شش ماهه داشته است. اما فراتر از یک اصل موضوع، بازار سهام جای نگرانی زیادی دارد زیرا بانک دیگری به تازگی سقوط کرده است. طبق گزارش ها، اولین بانک جمهوری، one از 20 بانک بزرگ ایالات متحده، قرار است در 28 آوریل توسط شرکت بیمه سپرده فدرال (FDIC) تصاحب شود. "دیگر وقت" برای نجات بخش خصوصی نبود. در اوایل سال جاری، بانک های سیلیکون ولی، بانک سیلورگیت و بانک سیگنچر شکست خوردند زیرا کل ایالات متحده با بحران بانکی در سه ماهه اول مواجه شد. بازار سهام تأثیرات مشابهی را متحمل شد که طی یک ماه، SPX نزدیک به 344.63 واحد کاهش یافت و 8.25 درصد کاهش یافت. اکنون با شروع ماه می پس از بحران بانک های فرست ریپابلیک، فدرال رزرو نیز قرار است جلسه کمیته بازار باز فدرال (FOMC) خود را در تاریخ 2 تا 3 می برگزار کند. در این جلسه، افزایش بعدی نرخ بهره انجام شد و فدرال رزرو به احتمال زیاد نرخ ها را 25 واحد پایه (bps) افزایش می دهد. احتمال همین در حال حاضر 80 درصد است که از 75 درصدی که چند روز پیش پس از انتشار گزارشهایی مبنی بر تصاحب First Republic Bank توسط دولت ایالات متحده مشاهده شد، افزایش یافته است. همه این موارد میتوانند تأثیر نزولی بر بازارهای سهام داشته باشند و به تأثیر صعودی بر قیمت Bitcoin تبدیل شوند. Bitcoin قیمت ممکن است افزایش یابد Bitcoin قیمت در گذشته واکنش نسبتاً غافلگیرکننده ای نه تنها به کاهش بازار سهام بلکه به بحران بانکی نیز داشته است. در حالی که سقوط بانک ها در سه ماهه اول سال در مجموع بازار سهام و کریپتو را در ابتدا کاهش داد، BTC خیلی زود پس از آن شروع به رشد کردند و طی ده روز آینده، بزرگترین ارز دیجیتال در جهان تا 40 درصد رشد کرد. این به این دلیل است که در اواخر سال 2022، Bitcoin خود را از بازار سهام جدا کرد و وضعیت "بهشت امن" و برچسب "حفاظ تورمی" مشابه طلا را به دست آورد. حتی در این هفته، با رسیدن گزارش های اولیه از شکست First Republic Banks، BTC نزدیک به 8 درصد افزایش یافت. بنابراین از آنجایی که روند «فروش در ماه مه» شکل میگیرد و عملکرد بازار سهام پایینتر از سطح است، قیمت Bitcoin فضایی برای استقبال از معاملهگران و سرمایهگذاران از دنیای سهام داشت. علاوه بر این، Bitcoin سودآوری عرضه هنوز بسیار پایین است و 74٪ است. در حالی که سودآوری طی چهار ماه گذشته از 45 درصد به بالاترین میزان در 12 ماه گذشته افزایش یافته است، اما هنوز فرصتی برای رشد وجود دارد تا قبل از مشاهده اوج بازار. معمولاً وقتی بیش از 95 درصد عرضه سودآور می شود، بالای بازار مشخص می شود که باعث فشار فروش می شود. تا آن زمان، BTC برای نمودار سود خوب است. نتیجه با نگاهی به شرایط گسترده تر بازار، به نظر می رسد که برای قیمت Bitcoin به طور بالقوه برخی شمعدان سبز در نمودارها مشاهده شود. این است مگر اینکه فصل جایگزین فراگیر شود و تسلط بیت کوین از 48.63 درصد فعلی به کمتر از 40 درصد کاهش یابد. در عین حال، معامله گران و سرمایه گذاران نیز باید مراقب افزایش نرخ بهره آتی باشند، زیرا افزایش بیش از 25 واحدی در ثانیه می تواند باعث سقوط قیمت شود.

thunderpips

BTC USD FUNDAMENTAL ANALYSIS

قیمت Bitcoin اخیراً از بازار سهام جدا شده است که در نتیجه آن حتی بحران بانکی اخیر تأثیری نزولی بر ارز دیجیتال نداشته است. اکنون با بازگشت روند "فروش در ماه مه"، این احتمال وجود دارد که BTC از مزایای بازار سهام با رشد آهسته بهره مند شود. "فروش در ماه مه" - سقوط بانک ها راه را هموار می کند در بازار سهام، با پایان ماه آوریل، یک ضرب المثل رایج در بین سرمایه گذاران زنده می شود - "در ماه می بفروش و برو. این اصل برای نشان دادن آغاز بدترین شش ماه سال برای معامله گران و سرمایه گذاران استفاده می شود. با توجه به عملکرد نسبتاً وحشتناک بازار سهام، یعنی شاخص S&P 500 (SPX)، "فروش در ماه می" پیشنهاد می کند به سادگی شش ماه آینده را نادیده بگیرید و دوباره در اکتبر بازگردید. در حالی که ممکن است مد دیگری به نظر برسد، اما از نظر تاریخی درستی این گفته ثابت شده است. بر اساس گزارشی از کارسون، به طور متوسط دوره می تا اکتبر کمترین رشد 1.7 درصدی را در مقایسه با سایر ترکیبات شش ماهه داشته است. اما فراتر از یک اصل موضوع، بازار سهام جای نگرانی زیادی دارد زیرا بانک دیگری به تازگی سقوط کرده است. طبق گزارش ها، اولین بانک جمهوری، one از 20 بانک بزرگ ایالات متحده، قرار است در 28 آوریل توسط شرکت بیمه سپرده فدرال (FDIC) تصاحب شود. "دیگر وقت" برای نجات بخش خصوصی نبود. در اوایل سال جاری، بانک های سیلیکون ولی، بانک سیلورگیت و بانک سیگنچر شکست خوردند زیرا کل ایالات متحده با بحران بانکی در سه ماهه اول مواجه شد. بازار سهام تأثیرات مشابهی را متحمل شد که طی یک ماه، SPX نزدیک به 344.63 واحد کاهش یافت و 8.25 درصد کاهش یافت. اکنون با شروع ماه می پس از بحران بانک های فرست ریپابلیک، فدرال رزرو نیز قرار است جلسه کمیته بازار باز فدرال (FOMC) خود را در تاریخ 2 تا 3 می برگزار کند. در این جلسه، افزایش بعدی نرخ بهره انجام شد و فدرال رزرو به احتمال زیاد نرخ ها را 25 واحد پایه (bps) افزایش می دهد. احتمال همین در حال حاضر 80 درصد است که از 75 درصدی که چند روز پیش پس از انتشار گزارشهایی مبنی بر تصاحب First Republic Bank توسط دولت ایالات متحده مشاهده شد، افزایش یافته است. همه این موارد میتوانند تأثیر نزولی بر بازارهای سهام داشته باشند و به تأثیر صعودی بر قیمت Bitcoin تبدیل شوند. Bitcoin قیمت ممکن است افزایش یابد Bitcoin قیمت در گذشته واکنش نسبتاً غافلگیرکننده ای نه تنها به کاهش بازار سهام بلکه به بحران بانکی نیز داشته است. در حالی که سقوط بانک ها در سه ماهه اول سال در مجموع بازار سهام و کریپتو را در ابتدا کاهش داد، BTC خیلی زود پس از آن شروع به رشد کردند و طی ده روز آینده، بزرگترین ارز دیجیتال در جهان تا 40 درصد رشد کرد. این به این دلیل است که در اواخر سال 2022، Bitcoin خود را از بازار سهام جدا کرد و وضعیت "بهشت امن" و برچسب "حفاظ تورمی" مشابه طلا را به دست آورد. حتی در این هفته، با رسیدن گزارش های اولیه از شکست First Republic Banks، BTC نزدیک به 8 درصد افزایش یافت. بنابراین از آنجایی که روند «فروش در ماه مه» شکل میگیرد و عملکرد بازار سهام پایینتر از سطح است، قیمت Bitcoin فضایی برای استقبال از معاملهگران و سرمایهگذاران از دنیای سهام داشت. علاوه بر این، Bitcoin سودآوری عرضه هنوز بسیار پایین است و 74٪ است. در حالی که سودآوری طی چهار ماه گذشته از 45 درصد به بالاترین میزان در 12 ماه گذشته افزایش یافته است، اما هنوز فرصتی برای رشد وجود دارد تا قبل از مشاهده اوج بازار. معمولاً وقتی بیش از 95 درصد عرضه سودآور می شود، بالای بازار مشخص می شود که باعث فشار فروش می شود. تا آن زمان، BTC برای نمودار سود خوب است. نتیجه با نگاهی به شرایط گسترده تر بازار، به نظر می رسد که برای قیمت Bitcoin به طور بالقوه برخی شمعدان سبز در نمودارها مشاهده شود. این است مگر اینکه فصل جایگزین فراگیر شود و تسلط بیت کوین از 48.63 درصد فعلی به کمتر از 40 درصد کاهش یابد. در عین حال، معامله گران و سرمایه گذاران نیز باید مراقب افزایش نرخ بهره آتی باشند، زیرا افزایش بیش از 25 واحدی در ثانیه می تواند باعث سقوط قیمت شود.

thunderpips

BTC USD FUNDAMENTAL ANALYSIS

قیمت Bitcoin اخیراً از بازار سهام جدا شده است که در نتیجه آن حتی بحران بانکی اخیر تأثیری نزولی بر ارز دیجیتال نداشته است. اکنون با بازگشت روند "فروش در ماه مه"، این احتمال وجود دارد که BTC از مزایای بازار سهام با رشد آهسته بهره مند شود. "فروش در ماه مه" - سقوط بانک ها راه را هموار می کند در بازار سهام، با پایان ماه آوریل، یک ضرب المثل رایج در بین سرمایه گذاران زنده می شود - "در ماه می بفروش و برو. این اصل برای نشان دادن آغاز بدترین شش ماه سال برای معامله گران و سرمایه گذاران استفاده می شود. با توجه به عملکرد نسبتاً وحشتناک بازار سهام، یعنی شاخص S&P 500 (SPX)، "فروش در ماه می" پیشنهاد می کند به سادگی شش ماه آینده را نادیده بگیرید و دوباره در اکتبر بازگردید. در حالی که ممکن است مد دیگری به نظر برسد، اما از نظر تاریخی درستی این گفته ثابت شده است. بر اساس گزارشی از کارسون، به طور متوسط دوره می تا اکتبر کمترین رشد 1.7 درصدی را در مقایسه با سایر ترکیبات شش ماهه داشته است. اما فراتر از یک اصل موضوع، بازار سهام جای نگرانی زیادی دارد زیرا بانک دیگری به تازگی سقوط کرده است. طبق گزارش ها، اولین بانک جمهوری، one از 20 بانک بزرگ ایالات متحده، قرار است در 28 آوریل توسط شرکت بیمه سپرده فدرال (FDIC) تصاحب شود. "دیگر وقت" برای نجات بخش خصوصی نبود. در اوایل سال جاری، بانک های سیلیکون ولی، بانک سیلورگیت و بانک سیگنچر شکست خوردند زیرا کل ایالات متحده با بحران بانکی در سه ماهه اول مواجه شد. بازار سهام تأثیرات مشابهی را متحمل شد که طی یک ماه، SPX نزدیک به 344.63 واحد کاهش یافت و 8.25 درصد کاهش یافت. اکنون با شروع ماه می پس از بحران بانک های فرست ریپابلیک، فدرال رزرو نیز قرار است جلسه کمیته بازار باز فدرال (FOMC) خود را در تاریخ 2 تا 3 می برگزار کند. در این جلسه، افزایش بعدی نرخ بهره انجام شد و فدرال رزرو به احتمال زیاد نرخ ها را 25 واحد پایه (bps) افزایش می دهد. احتمال همین در حال حاضر 80 درصد است که از 75 درصدی که چند روز پیش پس از انتشار گزارشهایی مبنی بر تصاحب First Republic Bank توسط دولت ایالات متحده مشاهده شد، افزایش یافته است. همه این موارد میتوانند تأثیر نزولی بر بازارهای سهام داشته باشند و به تأثیر صعودی بر قیمت Bitcoin تبدیل شوند. Bitcoin قیمت ممکن است افزایش یابد Bitcoin قیمت در گذشته واکنش نسبتاً غافلگیرکننده ای نه تنها به کاهش بازار سهام بلکه به بحران بانکی نیز داشته است. در حالی که سقوط بانک ها در سه ماهه اول سال در مجموع بازار سهام و کریپتو را در ابتدا کاهش داد، BTC خیلی زود پس از آن شروع به رشد کردند و طی ده روز آینده، بزرگترین ارز دیجیتال در جهان تا 40 درصد رشد کرد. این به این دلیل است که در اواخر سال 2022، Bitcoin خود را از بازار سهام جدا کرد و وضعیت "بهشت امن" و برچسب "حفاظ تورمی" مشابه طلا را به دست آورد. حتی در این هفته، با رسیدن گزارش های اولیه از شکست First Republic Banks، BTC نزدیک به 8 درصد افزایش یافت. بنابراین از آنجایی که روند «فروش در ماه مه» شکل میگیرد و عملکرد بازار سهام پایینتر از سطح است، قیمت Bitcoin فضایی برای استقبال از معاملهگران و سرمایهگذاران از دنیای سهام داشت. علاوه بر این، Bitcoin سودآوری عرضه هنوز بسیار پایین است و 74٪ است. در حالی که سودآوری طی چهار ماه گذشته از 45 درصد به بالاترین میزان در 12 ماه گذشته افزایش یافته است، اما هنوز فرصتی برای رشد وجود دارد تا قبل از مشاهده اوج بازار. معمولاً وقتی بیش از 95 درصد عرضه سودآور می شود، بالای بازار مشخص می شود که باعث فشار فروش می شود. تا آن زمان، BTC برای نمودار سود خوب است. نتیجه با نگاهی به شرایط گسترده تر بازار، به نظر می رسد که برای قیمت Bitcoin به طور بالقوه برخی شمعدان سبز در نمودارها مشاهده شود. این است مگر اینکه فصل جایگزین فراگیر شود و تسلط بیت کوین از 48.63 درصد فعلی به کمتر از 40 درصد کاهش یابد. در عین حال، معامله گران و سرمایه گذاران نیز باید مراقب افزایش نرخ بهره آتی باشند، زیرا افزایش بیش از 25 واحدی در ثانیه می تواند باعث سقوط قیمت شود.

thunderpips

BTC USDT BUY (BITCOIN - TETHER US)

سلام. قیمت به طور ناگهانی به سمت صعود حرکت می کند. منتظر بمانید تا قیمت یک الگوی ادامه ایجاد کند و برای خرید، اقدام قیمت strong را تماشا کنید.

سلب مسئولیت

هر محتوا و مطالب مندرج در سایت و کانالهای رسمی ارتباطی سهمتو، جمعبندی نظرات و تحلیلهای شخصی و غیر تعهد آور بوده و هیچگونه توصیهای مبنی بر خرید، فروش، ورود و یا خروج از بازارهای مالی نمی باشد. همچنین کلیه اخبار و تحلیلهای مندرج در سایت و کانالها، صرفا بازنشر اطلاعات از منابع رسمی و غیر رسمی داخلی و خارجی است و بدیهی است استفاده کنندگان محتوای مذکور، مسئول پیگیری و حصول اطمینان از اصالت و درستی مطالب هستند. از این رو ضمن سلب مسئولیت اعلام میدارد مسئولیت هرنوع تصمیم گیری و اقدام و سود و زیان احتمالی در بازار سرمایه و ارز دیجیتال، با شخص معامله گر است.